SUMMARY

The euro crisis was fuelled by the diabolic loop between sovereign risk and bank risk, coupled with cross-border flight-to-safety capital flows. European Safe Bonds (ESBies), a euro area-wide safe asset without joint liability, would help to resolve these problems. We make three contributions. First, numerical simulations show that ESBies with a subordination level of 30% would be as safe as German bunds and would increase safe asset supply. Second, a model shows how, when and why the two features of ESBies – diversification and seniority – can weaken the diabolic loop and its diffusion across countries. Third, we propose how to create ESBies, starting with limited issuance by public or private-sector entities.

1. INTRODUCTION

The creation of the euro in 1999 was a landmark in the European integration process. Since 2009, however, the euro area has been roiled by financial crisis, with heightened sovereign default risk, a weakened banking sector, and a stagnating macroeconomy.

Why did this happen? Among many factors, the euro area lacked institutional features necessary for the success of a monetary union, including emergency funding for sovereigns and common banking supervision and resolution (Brunnermeier et al., 2016). Some of these deficiencies have since been addressed, but one crucial feature remains missing. The euro area does not supply a union-wide safe asset, i.e. one that yields the same pay-off at any point in time and state of the world (Section 2). By storing value in safe assets, rather than the risky debt of the nation-state in which they reside, banks would weaken the diabolic loop between their solvency and that of their domestic government. In a cross-border currency area, union-wide safe assets ensure that flight-to-safety capital flows occur across assets (i.e. from risky to risk-free assets) rather than countries.

To fill this gap, Brunnermeier et al. (2011) propose Sovereign Bond-Backed Securities (SBBSs), which constitute senior and junior claims on a diversified portfolio of euro area central government (‘sovereign’) bonds (Section 3). SBBSs are politically feasible as they entail no joint liability among sovereigns, in contrast to most other proposals.1 Governments remain responsible for servicing their own debt, which trades at a market price, exerting discipline on borrowing decisions. One government could default on its obligations without others bearing any bail-out responsibility and without holders of the senior claim bearing any losses.

We advocate Brunnermeier et al.’s proposal in three ways. First, in Section 4, simulations measure SBBSs’ risk. With a subordination level of 30%, the senior claim has an expected loss rate similar to that of German bunds. This motivates the moniker of ‘European Safe Bonds’ (or ‘ESBies’) to refer to the senior claim. In addition, ESBies would increase the supply of safe assets relative to the status quo. The corresponding junior claim — which we refer to as ‘European Junior Bonds’ (or ‘EJBies’) — would be attractive investments, thanks to their embedded leverage and expected loss rates similar to those of riskier euro area sovereign bonds.

These simulations take default probabilities as given, yet probabilities should change endogenously in response to banks’ safer portfolios. To capture this idea, in Section 5, we extend a workhorse model of the diabolic loop between sovereign risk and bank risk developed by Brunnermeier et al. (2016). We show that the diabolic loop is less likely to arise if banks hold adequately subordinated ESBies rather than domestic government debt or a diversified portfolio with no tranching. ESBies are thus a ‘positive sum game’.

Third, in Sections 6 and 7, we investigate how to implement ESBies. At present, their creation is stymied by regulation, which would penalize them relative to direct holdings of sovereign bonds. To remove this regulatory roadblock, policy-makers should ensure a fair treatment of ESBies, and provide incentives for greater diversification of banks’ and insurers’ government debt portfolios. Policy should also play a standard-setting role, helping financial institutions to overcome coordination failures in creating a new market. An official Handbook should define ESBies’ subordination level and underlying portfolio composition, as well as the institution(s) licensed to issue them. Following these preparatory steps, issuance should start at a small scale, allowing investors to digest the new securities, before the market for ESBies is deepened.

2. CRISIS WITHOUT A UNION-WIDE SAFE ASSET

Modern financial systems rely on safe assets. They lubricate financial transactions, which often entail a contractual requirement to post collateral (Giovannini, 2013), and so allow market participants to transfer liquidity or market risk without creating counterparty credit risk. To comply with liquidity regulations, banks need to hold safe assets to meet their funding needs in a stress scenario (Basel Committee on Banking Supervision, 2013). And central banks conduct monetary policy by exchanging money, whether currency or reserves, for quasi-money in the form of safe assets with longer maturities (Brunnermeier and Sannikov, 2016).

A safe asset is liquid, maintains value during crises, and is denominated in a currency with stable purchasing power. Relative to investors’ demand for safe assets, there is scarce global supply of securities that possess all three characteristics (Caballero, 2010). The most widely held safe asset, US Treasury bills and bonds, earns a large ‘safe haven’ premium of 0.7% per year on average (Krishnamurthy and Vissing-Jorgensen, 2012). Acute safe asset scarcity can have negative macroeconomic effects by increasing risk premia, pushing the economy into a ‘safety trap’ (Caballero et al., 2016).

The euro area does not supply a safe asset on par with the United States, despite encompassing a similarly large economy and developed financial markets. Instead, euro area governments issue debt with heterogeneous risk and liquidity characteristics. Five euro area nation-states – Germany, the Netherlands, Austria, Finland and Luxembourg – are rated triple-A by either Moody’s or S&P. In 2015, the face value of central government debt securities issued by these nation-states stood at €1.9tn (18% of euro area GDP). By contrast, outstanding central government debt securities issued by the United States had a face value of $11.7tn in 2015 (65% of US GDP). The relative scarcity and asymmetric supply of euro-denominated safe assets creates two problems, which we explain next.

2.1. Diabolic loop

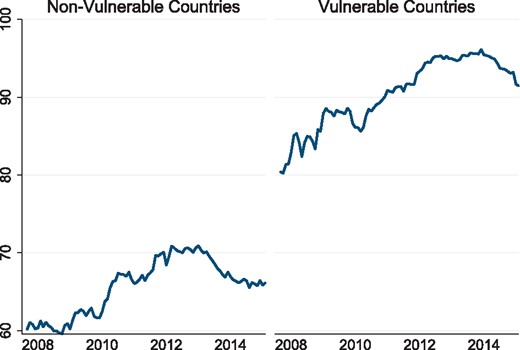

Mean of banks’ domestic sovereign bond holdings as a percentage of their total holdings

Notes: Figure plots the mean of euro area banks’ holdings of their own sovereign’s debt as a proportion of their total sovereign debt holdings. Banks are split into two subsamples: those resident in ‘non-vulnerable’ countries (i.e. Austria, Belgium, Germany, Estonia, Finland, France, Luxembourg, Malta, the Netherlands) and those in ‘vulnerable’ countries (i.e. Spain, Ireland, Italy, Portugal, Cyprus, Slovenia, Greece).

Sources: ECB; Altavilla et al. (2016).

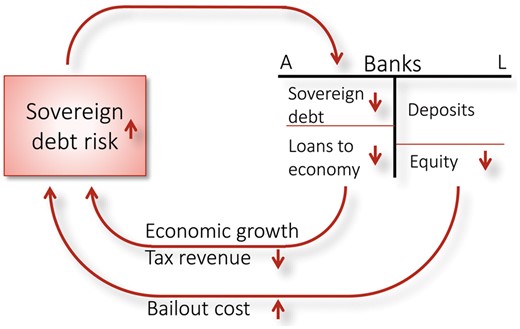

The sovereign-bank diabolic loop

Notes: Figure depicts the diabolic loop between sovereign risk and bank risk. The first loop operates via a bail-out channel: the reduction in banks’ solvency raises the probability of a bail-out, increasing sovereign risk and lowering bond prices. The second loop operates via the real economy: the reduction in banks’ solvency owing to the fall in sovereign bond prices prompts them to cut lending – reducing real activity, lowering tax revenues and increasing sovereign risk further.

Source: Brunnermeier et al. (2011).

This loop was the quintessential characteristic of the euro area sovereign debt crisis. In some countries (e.g. Ireland and Spain), widespread bank insolvencies endangered the sustainability of sovereign debt dynamics. In other countries – Greece, Italy, Portugal and Belgium – long-run public debt accumulation and slow growth generated sovereign debt dynamics that threatened banks’ solvency. In both cases, domestic governments’ guarantees became less credible, and the interaction of sovereign risk and bank risk amplified the crisis after 2009. To weaken the diabolic loop, the euro area needs a safe asset that banks can hold without being exposed to domestic sovereign risk.

2.2. Flight to safety

The euro area features a strong asymmetry in the provision of safe assets: Germany supplies two-thirds of top-rated euro-denominated central government debt securities. This asymmetry exacerbates the swings of cross-border capital flows during financial crises.

During the 2003–2007 boom, capital flowed from non-vulnerable to vulnerable countries, attracted by the perceived relative abundance of investment opportunities and the absence of foreign exchange risk. These boom-era capital flows fuelled credit expansion in vulnerable countries, raising local asset prices and compressing sovereign bond spreads. Effectively, investors treated all euro area nation-states’ bonds as safe. In the presence of financial frictions, however, the credit expansion in vulnerable countries led to an appreciation of the real exchange rate. Productivity slumped because extra credit was disproportionately allocated to low-value-added sectors (Reis, 2013), especially real estate and other non-tradable sectors (Benigno and Fornaro, 2014).

After 2009, short-term capital flows from non-vulnerable to vulnerable countries reversed, as investors sought safety above all else (Lane, 2013). Without a union-wide safe asset, non-vulnerable sovereigns’ debt partially satisfied investors’ newfound demand for safety. The capital flow reversal depressed non-vulnerable nation-states’ borrowing costs below the level justified by fundamentals – and, in proportion, elevated vulnerable sovereigns’ borrowing costs. Consequently, capital in search of safety flowed from high-risk to low-risk countries in a self-fulfilling manner.

With ESBies, capital flights to safety would take place from high-risk to low-risk European assets rather than from vulnerable to non-vulnerable countries. As a result, the safe haven premium enjoyed during crises by the euro area’s pre-eminent safe asset – German bunds – would dissipate. This dissipation is desirable: Germany’s safe haven premium is the corollary of expectations-driven runs on sovereign debt elsewhere in the euro area. From a German point of view, the loss of the safe haven premium would be compensated in two ways. First, ESBies would reduce the probability of crises, as we show in Section 5. Crises are particularly damaging for Germany’s export-oriented economy, regardless of the safe haven premium. Second, conditional on being in a crisis, bail-out requirements would be smaller if banks’ portfolios were invested in ESBies, as they would be less exposed to sovereign risk. This benefits fiscally strong countries that might otherwise contribute disproportionately to a bail-out.

3. DESIGN OF ESBies

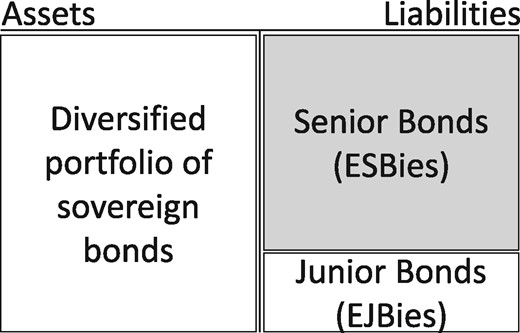

ESBies are the senior claim on a diversified portfolio of euro area sovereign bonds. To create them, a public or private special purpose entity (or entities) purchases a diversified portfolio of euro area sovereign bonds,2 weighted according to a moving average of euro area countries’ GDPs or contributions to European Central Bank (ECB) capital.3 For investors, a well-defined, slow-moving weighting scheme has the benefit of transparency and predictability. More importantly, the use of GDP or ECB capital key weights ensures that there are no perverse incentives for governments in terms of debt issuance: the special purpose entity or entities would buy only a certain fraction of each country’s outstanding central government debt securities at their market price. Countries with large debt stocks would need to place proportionally more of their obligations in the open market.4

Balance sheet of an SBBS securitization vehicle

Notes: Figure shows the balance sheet of an SBBS securitization vehicle, whereby its diversified portfolio of sovereign bonds is financed by the issuance of two securities, with ESBies senior to EJBies.

Both tranching and diversification are key to ESBies’ safety. Losses arising from sovereign defaults would first be borne by holders of the junior bond; only if they exceed the subordination level, such that EJBies are entirely wiped out, would ESBies begin to take any losses. In Section 4, we show that a subordination level of 30% – such that the junior bond represents 30%, and the senior bond 70%, of the underlying face value – would ensure that ESBies have an expected loss rate similar to that of German bunds. As such, ESBies would be standard low-risk fixed income securities; EJBies would be more akin to government equity with a state-contingent pay-off structure. The next sections explore the quantitative properties of ESBies and EJBies, their effect on the diabolic loop, and their practical implementation.

4. QUANTITATIVE PROPERTIES OF ESBies

This section addresses three related questions. Would ESBies be as safe as top-rated sovereign bonds? Would their supply be adequate for banks to use them as a safe store of value? And would there be enough demand for EJBies? The simulation results lead us to answer ‘yes’ to all three questions. First, with an appropriate subordination level, ESBies can be designed such that they are as safe as German sovereign bonds. Second, ESBies could substantially increase the supply of safe assets relative to the status quo, without deviating from the fundamental principle that they should be backed by the sovereign bonds of all euro area Member States (with the exception of those which have lost primary market access, as we explain in Subsection 6.2.3). Third, in our benchmark calibration, EJBies have an expected loss rate comparable to those of vulnerable euro area sovereign bonds.

We obtain these results by comparing four security designs: (i) the status quo, in which sovereign bonds are neither pooled across nation-states nor tranched for safety; (ii) national tranching, where each sovereign bond is tranched into a senior and junior component at a given subordination level; (iii) pure pooling, where sovereign bonds are pooled in a single portfolio, with weights equal to countries’ relative GDP over 2010–2014; and (iv) pooling and tranching, where the pooled portfolio is tranched into a senior component (ESBies) and a junior component (EJBies) at a given subordination level.

We begin with a simple calculation to illustrate ESBies’ robustness to extreme default scenarios (Subsection 4.1). We then undertake a more rigorous analysis by way of numerical simulations (Subsection 4.2). Under a benchmark calibration of the simulation model, ESBies with a subordination level of 30% are as safe as German bunds (Subsection 4.3). To check the sensitivity of these results to parameter uncertainty, which is a perennial concern when measuring the risk of securitizations (Antoniades and Tarashev, 2014), we subject the simulation model to an adverse calibration in Subsection 4.4 and a battery of alternative parameterizations in a separate Web Appendix.

These simulations take the distribution of default and loss-given-default (LGD) rates as given, and therefore, ignore general equilibrium effects. Yet by expanding the volume of safe assets that may be held by banks, ESBies endogenously reduce the number of states in which the diabolic loop can operate. Because this mechanism is hard to quantify empirically, Section 5 presents a theoretical model that captures it. For now, though, by neglecting this general equilibrium effect, our simulations are conservative in the sense that they understate the risk reduction that ESBies can achieve.

4.1. Illustrative default scenarios

Sovereign defaults are rare events, implying considerable uncertainty regarding true LGD rates. For robustness, we subject sovereign bonds to three different LGD rates per country i: and . The values of , which represent the most severe losses, are shown in Table 1; the values of are 80% those of ; and values are 50% lower.

Simulation inputs

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Rating | C. Bonds/GDP | G. Debt/GDP | Weight | pd1 | pd2 | pd3 | lgd1 | |

| Germany | 1 | 39 | 71 | 28.16 | 5 | 0.5 | 0 | 40 |

| The Netherlands | 1 | 51 | 65 | 6.61 | 10 | 1 | 0 | 40 |

| Luxembourg | 1 | 12 | 22 | 0.18 | 10 | 1 | 0 | 40 |

| Austria | 1.5 | 67 | 86 | 3.21 | 15 | 2 | 0 | 45 |

| Finland | 1.5 | 48 | 64 | 2.02 | 15 | 2 | 0 | 45 |

| France | 3 | 73 | 96 | 21.25 | 25 | 3 | 0.05 | 60 |

| Belgium | 3.5 | 84 | 106 | 3.93 | 30 | 4 | 0.1 | 62.5 |

| Estonia | 4.5 | 0 | 10 | 0.03 | 35 | 5 | 0.1 | 67.5 |

| Slovakia | 5 | 45 | 52 | 0.66 | 35 | 6 | 0.1 | 70 |

| Ireland | 6.5 | 49 | 79 | 1.80 | 40 | 6 | 0.12 | 75 |

| Latvia | 7 | 25 | 36 | 0.17 | 50 | 10 | 0.3 | 75 |

| Lithuania | 7 | 34 | 43 | 0.25 | 50 | 10 | 0.3 | 75 |

| Malta | 7.5 | 56 | 61 | 0.07 | 55 | 11 | 0.4 | 78 |

| Slovenia | 9 | 71 | 83 | 0.37 | 60 | 15 | 0.4 | 80 |

| Spain | 9 | 79 | 100 | 10.77 | 60 | 15 | 0.4 | 80 |

| Italy | 9.5 | 110 | 132 | 16.52 | 65 | 18 | 0.5 | 80 |

| Portugal | 12 | 72 | 129 | 1.77 | 70 | 30 | 2.5 | 85 |

| Cyprus | 13.5 | 35 | 108 | 0.19 | 75 | 40 | 10 | 87.5 |

| Greece | 19 | 40 | 177 | 2.01 | 95 | 75 | 45 | 95 |

| Average | 4.6 | 66 | 93 | 31.30 | 8.07 | 1.12 | 59.47 | |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Rating | C. Bonds/GDP | G. Debt/GDP | Weight | pd1 | pd2 | pd3 | lgd1 | |

| Germany | 1 | 39 | 71 | 28.16 | 5 | 0.5 | 0 | 40 |

| The Netherlands | 1 | 51 | 65 | 6.61 | 10 | 1 | 0 | 40 |

| Luxembourg | 1 | 12 | 22 | 0.18 | 10 | 1 | 0 | 40 |

| Austria | 1.5 | 67 | 86 | 3.21 | 15 | 2 | 0 | 45 |

| Finland | 1.5 | 48 | 64 | 2.02 | 15 | 2 | 0 | 45 |

| France | 3 | 73 | 96 | 21.25 | 25 | 3 | 0.05 | 60 |

| Belgium | 3.5 | 84 | 106 | 3.93 | 30 | 4 | 0.1 | 62.5 |

| Estonia | 4.5 | 0 | 10 | 0.03 | 35 | 5 | 0.1 | 67.5 |

| Slovakia | 5 | 45 | 52 | 0.66 | 35 | 6 | 0.1 | 70 |

| Ireland | 6.5 | 49 | 79 | 1.80 | 40 | 6 | 0.12 | 75 |

| Latvia | 7 | 25 | 36 | 0.17 | 50 | 10 | 0.3 | 75 |

| Lithuania | 7 | 34 | 43 | 0.25 | 50 | 10 | 0.3 | 75 |

| Malta | 7.5 | 56 | 61 | 0.07 | 55 | 11 | 0.4 | 78 |

| Slovenia | 9 | 71 | 83 | 0.37 | 60 | 15 | 0.4 | 80 |

| Spain | 9 | 79 | 100 | 10.77 | 60 | 15 | 0.4 | 80 |

| Italy | 9.5 | 110 | 132 | 16.52 | 65 | 18 | 0.5 | 80 |

| Portugal | 12 | 72 | 129 | 1.77 | 70 | 30 | 2.5 | 85 |

| Cyprus | 13.5 | 35 | 108 | 0.19 | 75 | 40 | 10 | 87.5 |

| Greece | 19 | 40 | 177 | 2.01 | 95 | 75 | 45 | 95 |

| Average | 4.6 | 66 | 93 | 31.30 | 8.07 | 1.12 | 59.47 | |

Notes: This table reports the inputs used in the numerical simulations described in Section 4. Nation-states are ordered in terms of their sovereign credit ratings as of December 2015. Letter grades are converted into a numerical score (1 is AAA, 19 is CCC-) and averaged across S&P and Moody’s (column 1). Column 2 refers to the face value of outstanding central government debt securities as a percentage of GDP in Q4 2015 (Eurostat code: gov_10q_ggdebt). Column 3 refers to the face value of consolidated general government gross debt (following the Maastricht criteria) as a percentage of GDP in 2015 (Eurostat codes: teina225 and naida_10_gdp). Column 4 refers to the percentage weight of each sovereign in the pooled euro area portfolio, corresponding to nation-states’ relative GDPs (with the constraint that the pooled portfolio cannot include more than 100% of nation-states’ outstanding debt). Columns 5–7 describe the five-year default probabilities (in percentage) in states 1, 2 and 3, respectively. Column 8 describes the five-year LGD rates (in percentage) in state 1; in state 2, LGD rates are 80% of those in state 1 and in state 3 they are 50% of those in state 1.

Simulation inputs

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Rating | C. Bonds/GDP | G. Debt/GDP | Weight | pd1 | pd2 | pd3 | lgd1 | |

| Germany | 1 | 39 | 71 | 28.16 | 5 | 0.5 | 0 | 40 |

| The Netherlands | 1 | 51 | 65 | 6.61 | 10 | 1 | 0 | 40 |

| Luxembourg | 1 | 12 | 22 | 0.18 | 10 | 1 | 0 | 40 |

| Austria | 1.5 | 67 | 86 | 3.21 | 15 | 2 | 0 | 45 |

| Finland | 1.5 | 48 | 64 | 2.02 | 15 | 2 | 0 | 45 |

| France | 3 | 73 | 96 | 21.25 | 25 | 3 | 0.05 | 60 |

| Belgium | 3.5 | 84 | 106 | 3.93 | 30 | 4 | 0.1 | 62.5 |

| Estonia | 4.5 | 0 | 10 | 0.03 | 35 | 5 | 0.1 | 67.5 |

| Slovakia | 5 | 45 | 52 | 0.66 | 35 | 6 | 0.1 | 70 |

| Ireland | 6.5 | 49 | 79 | 1.80 | 40 | 6 | 0.12 | 75 |

| Latvia | 7 | 25 | 36 | 0.17 | 50 | 10 | 0.3 | 75 |

| Lithuania | 7 | 34 | 43 | 0.25 | 50 | 10 | 0.3 | 75 |

| Malta | 7.5 | 56 | 61 | 0.07 | 55 | 11 | 0.4 | 78 |

| Slovenia | 9 | 71 | 83 | 0.37 | 60 | 15 | 0.4 | 80 |

| Spain | 9 | 79 | 100 | 10.77 | 60 | 15 | 0.4 | 80 |

| Italy | 9.5 | 110 | 132 | 16.52 | 65 | 18 | 0.5 | 80 |

| Portugal | 12 | 72 | 129 | 1.77 | 70 | 30 | 2.5 | 85 |

| Cyprus | 13.5 | 35 | 108 | 0.19 | 75 | 40 | 10 | 87.5 |

| Greece | 19 | 40 | 177 | 2.01 | 95 | 75 | 45 | 95 |

| Average | 4.6 | 66 | 93 | 31.30 | 8.07 | 1.12 | 59.47 | |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Rating | C. Bonds/GDP | G. Debt/GDP | Weight | pd1 | pd2 | pd3 | lgd1 | |

| Germany | 1 | 39 | 71 | 28.16 | 5 | 0.5 | 0 | 40 |

| The Netherlands | 1 | 51 | 65 | 6.61 | 10 | 1 | 0 | 40 |

| Luxembourg | 1 | 12 | 22 | 0.18 | 10 | 1 | 0 | 40 |

| Austria | 1.5 | 67 | 86 | 3.21 | 15 | 2 | 0 | 45 |

| Finland | 1.5 | 48 | 64 | 2.02 | 15 | 2 | 0 | 45 |

| France | 3 | 73 | 96 | 21.25 | 25 | 3 | 0.05 | 60 |

| Belgium | 3.5 | 84 | 106 | 3.93 | 30 | 4 | 0.1 | 62.5 |

| Estonia | 4.5 | 0 | 10 | 0.03 | 35 | 5 | 0.1 | 67.5 |

| Slovakia | 5 | 45 | 52 | 0.66 | 35 | 6 | 0.1 | 70 |

| Ireland | 6.5 | 49 | 79 | 1.80 | 40 | 6 | 0.12 | 75 |

| Latvia | 7 | 25 | 36 | 0.17 | 50 | 10 | 0.3 | 75 |

| Lithuania | 7 | 34 | 43 | 0.25 | 50 | 10 | 0.3 | 75 |

| Malta | 7.5 | 56 | 61 | 0.07 | 55 | 11 | 0.4 | 78 |

| Slovenia | 9 | 71 | 83 | 0.37 | 60 | 15 | 0.4 | 80 |

| Spain | 9 | 79 | 100 | 10.77 | 60 | 15 | 0.4 | 80 |

| Italy | 9.5 | 110 | 132 | 16.52 | 65 | 18 | 0.5 | 80 |

| Portugal | 12 | 72 | 129 | 1.77 | 70 | 30 | 2.5 | 85 |

| Cyprus | 13.5 | 35 | 108 | 0.19 | 75 | 40 | 10 | 87.5 |

| Greece | 19 | 40 | 177 | 2.01 | 95 | 75 | 45 | 95 |

| Average | 4.6 | 66 | 93 | 31.30 | 8.07 | 1.12 | 59.47 | |

Notes: This table reports the inputs used in the numerical simulations described in Section 4. Nation-states are ordered in terms of their sovereign credit ratings as of December 2015. Letter grades are converted into a numerical score (1 is AAA, 19 is CCC-) and averaged across S&P and Moody’s (column 1). Column 2 refers to the face value of outstanding central government debt securities as a percentage of GDP in Q4 2015 (Eurostat code: gov_10q_ggdebt). Column 3 refers to the face value of consolidated general government gross debt (following the Maastricht criteria) as a percentage of GDP in 2015 (Eurostat codes: teina225 and naida_10_gdp). Column 4 refers to the percentage weight of each sovereign in the pooled euro area portfolio, corresponding to nation-states’ relative GDPs (with the constraint that the pooled portfolio cannot include more than 100% of nation-states’ outstanding debt). Columns 5–7 describe the five-year default probabilities (in percentage) in states 1, 2 and 3, respectively. Column 8 describes the five-year LGD rates (in percentage) in state 1; in state 2, LGD rates are 80% of those in state 1 and in state 3 they are 50% of those in state 1.

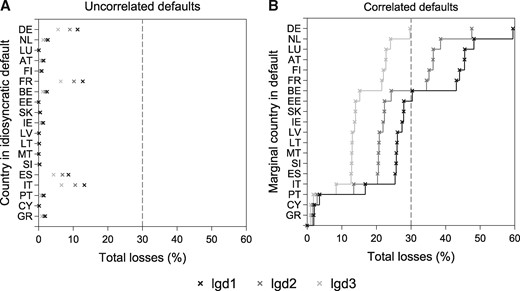

Illustrative default scenarios

Notes: Figure plots total losses incurred by a portfolio comprising euro area sovereign bonds with weights given in Table 1. Panel A plots total losses on this portfolio following uncorrelated, country-specific default events (under the respective LGD of and , shown in different shades of grey, and given in Table 1). Panel B plots total losses following simultaneous cross-country defaults: at any given point on the vertical axis, all countries at and below that point are assumed to be in default.

In Panel B of Figure 4, defaults are correlated across countries. At any given point on the vertical axis, all countries at and below that point are assumed to be in default, with loss rates given by their respective or . For example, the ‘ES’ point on the vertical axis refers to simultaneous defaults by Spain, Italy, Portugal, Cyprus and Greece: when this happens, the underlying portfolio incurs losses of 25.4%, 20.3% or 12.7% under assumptions of and , respectively. With , ESBies are robust to simultaneous defaults by Estonia and all nation-states rated below it; with , they are robust to defaults by France and all nation-states rated below it; with , they survive all defaults (i.e. ESBies incur no losses even if all nation-states default).

These illustrative calculations are informative regarding the severity of shocks that would be necessary for ESBies to begin to take any losses. Their usefulness is limited, however, as they consider a set of default events without specifying their probabilities. Therefore, in the next subsection, we subject ESBies and EJBies to an ex ante risk assessment in a simulation model, which takes thousands of draws from default probability distributions.

4.2. Simulating multiple default scenarios

To further assess the quantitative properties of ESBies and EJBies, we design a two-level hierarchical simulation model. In the first level, we simulate 2,000 five-year periods, in each of which the aggregate economic state can take one of three values:

State 1: A severe recession occurs; default and LGD rates are very high for all nation-states, and particularly for those with worse credit ratings. In this state, the expected default rate over five years is listed in column 5 of Table 1; LGD rates are shown in column 8.

State 2: A mild recession occurs; default and LGD rates are elevated in all nation-states. Expected five-year default rates are given in column 6 of Table 1; expected LGD rates are 80% of those in state 1.

State 3: The economy expands; default risk is low for most nation-states (column 7 of Table 1); LGD rates are 50% of those in state 1.

The aggregate random variable determines that the euro area economy is in the good state 70% of the time and in one of the two recessionary states 30% of the time. This 70:30 split between expansions and recessions accords with NBER data on the US business cycle spanning 1854–2010. Using CEPR’s business cycle dating for the euro area on the shorter sample of 1974–2014, the economy was in a recession in 20% of the years, so our assumption of 70:30 is appropriately pessimistic. Of the 30% recessionary states, similarly long time-series data gathered by Reinhart and Rogoff (2009) and Schularick and Taylor (2012) suggest that about one-sixth are severe. We match these historical patterns by assuming that mild recessions occur 25% of the time and severe recessions occur 5% of the time.

The model’s second hierarchical level concerns sovereign default. Within each five-year period, conditional on the aggregate state in that period (drawn in the first level of the model), we take 5,000 draws of the sovereigns’ stochastic default processes. The random variable that determines whether a given sovereign defaults, and which can be interpreted as the ‘sunspot’ in the theoretical model of Section 5, is assumed to have a fat-tailed distribution (Student’s t with four degrees of freedom), making defaults far more likely than under a normal distribution. In each state of the economy, nation-states’ default probabilities increase with their numerical credit score (higher scores indicate worse ratings). With 2,000 five-year periods and 5,000 draws within each period, our simulation uses a total of 10 million draws.

4.3. Benchmark calibration of the numerical simulation

The purpose of our simulations is to compare the four cases of security design along two dimensions: five-year expected loss rates (calculated as average loss rates over the simulations of the default process), and the ‘safe asset multiplier’ (namely the units of safe assets produced by the securitization per unit of safe asset in the underlying portfolio).

In the benchmark calibration of the model, we select the parameters such that average default rates are consistent with market prices. According to calculations by Deutsche Bank, which infers default probabilities from credit default swap (CDS) spreads by assuming a constant LGD rate of 40%, annual default probabilities were 0.20% for Germany and 0.30% for the Netherlands in December 2015; by comparison, our benchmark calibration of the model calculates 0.07 and 0.15%, respectively. This difference can be explained by the counterparty credit risk and liquidity premia that inflate CDS spreads, particularly for highly rated reference entities. For other countries, our model calculates precisely the same default probabilities as those implied by CDS spreads in December 2015. This cross-check with CDS spreads allows us to establish nation-states’ relative riskiness; in Subsection 4.4 and the Web Appendix, we subject default rates to various stress tests.

Moreover, the model is calibrated so that LGD rates are broadly consistent with historical data on recoveries following sovereign defaults. According to Moody’s data on sovereign defaults over 1983–2010, most of which were by emerging or developing economies, issuer-weighted LGD rates were 47% when measured by the post-default versus pre-distress trading price, and 33% based on the present value of cash flows received as a result of the distressed exchange compared with those initially promised. On a value-weighted basis, average LGD rates were 69% and 64%, respectively. This calibration is subject to further robustness checks in the Web Appendix, where we envisage a uniform 15% increase in LGD rates.

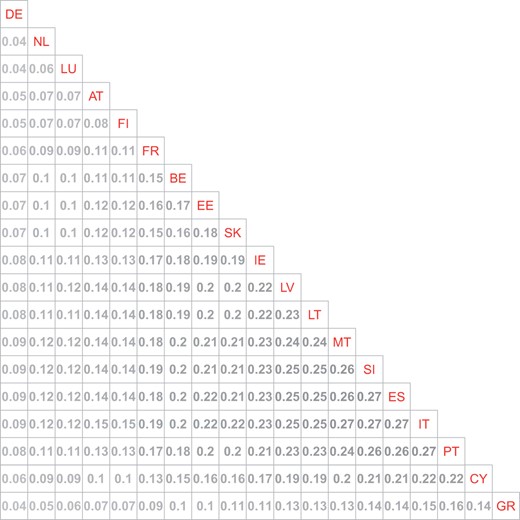

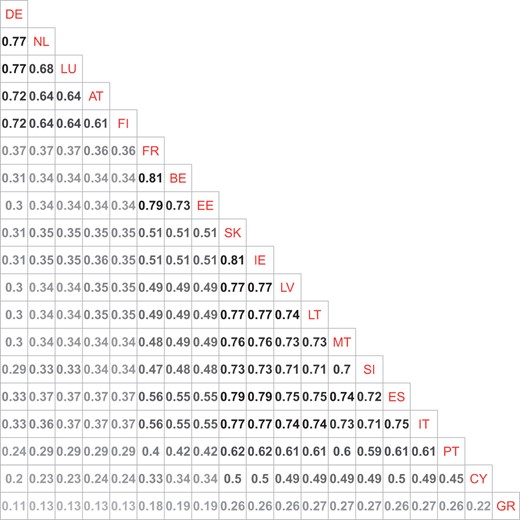

These calibrations deliver the default and LGD rates reported in Table 1, and the cross-country correlations in default probabilities shown in Panel A of Table 2. Later, in Subsection 4.4, we impose additional contagion assumptions that lead to the aggravated correlations shown in Panel B of Table 2. Even more severe contagion assumptions are modelled in the Web Appendix.

Correlations between nation-states’ default probabilities

| Panel A: Benchmark calibration | ||||||||||||||||||

| ||||||||||||||||||

| Panel B: Adverse calibration | ||||||||||||||||||

|

| Panel A: Benchmark calibration | ||||||||||||||||||

| ||||||||||||||||||

| Panel B: Adverse calibration | ||||||||||||||||||

|

Notes: Matrices show the correlations between nation-states’ probabilities of default in the benchmark (Panel A, described in Subsection 4.3) and adverse (Panel B, described in Subsection 4.4) calibrations of the simulation model. Correlations are much higher in the adverse calibration owing to the additional contagion assumptions. Higher (lower) correlations are shown in darker (lighter) gray.

Correlations between nation-states’ default probabilities

| Panel A: Benchmark calibration | ||||||||||||||||||

| ||||||||||||||||||

| Panel B: Adverse calibration | ||||||||||||||||||

|

| Panel A: Benchmark calibration | ||||||||||||||||||

| ||||||||||||||||||

| Panel B: Adverse calibration | ||||||||||||||||||

|

Notes: Matrices show the correlations between nation-states’ probabilities of default in the benchmark (Panel A, described in Subsection 4.3) and adverse (Panel B, described in Subsection 4.4) calibrations of the simulation model. Correlations are much higher in the adverse calibration owing to the additional contagion assumptions. Higher (lower) correlations are shown in darker (lighter) gray.

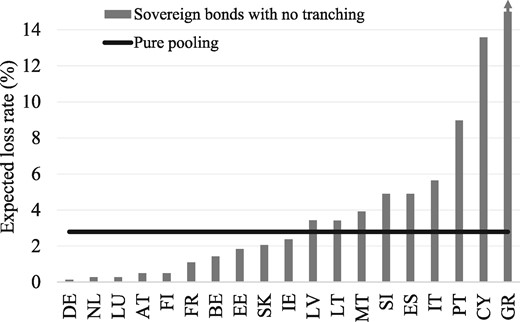

4.3.1. Effects of pooling and tranching on safety

Untranched bonds’ five-year expected loss rates

Notes: Figure shows the expected loss rates of national sovereign bonds versus that of the pooled euro area security without tranching. The vertical axis is truncated at 15% for presentational purposes; the expected loss rate on Greek sovereign bonds is 34.16%. The data presented in this figure correspond to those reported in Table 3.

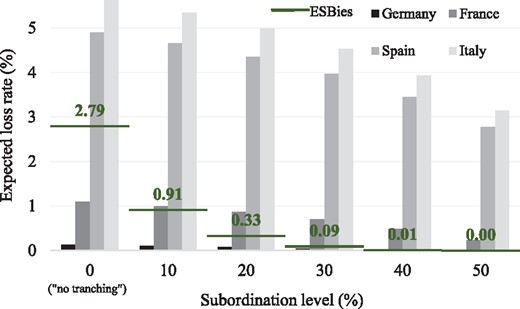

Senior bonds’ five-year expected loss rates by subordination level

Notes: Figure shows the expected loss rates of the senior tranche of national sovereign bonds versus that of the pooled euro area security. When the subordination level is 0%, there is no tranching: national sovereign bonds correspond to the status quo, and the pooled security corresponds to pure pooling (as in Figure 5). When the subordination level is greater than 0%, national sovereign bonds correspond to national tranching, and the pooled portfolio corresponds to ESBies. For brevity, this figure displays only the largest four nation-states; data for others are shown in Table 3.

Senior bonds’ five-year expected loss rates in the benchmark calibration (%)

| Subordination | 0% | 10% | 20% | 30% | 40% | 50% | 60% | 70% | 80% | 90% |

|---|---|---|---|---|---|---|---|---|---|---|

| Germany | 0.13 | 0.11 | 0.08 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| The Netherlands | 0.27 | 0.22 | 0.15 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Luxembourg | 0.27 | 0.22 | 0.15 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Austria | 0.50 | 0.42 | 0.32 | 0.19 | 0.06 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Finland | 0.50 | 0.42 | 0.32 | 0.19 | 0.06 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| France | 1.09 | 0.99 | 0.86 | 0.70 | 0.49 | 0.23 | 0.00 | 0.00 | 0.00 | 0.00 |

| Belgium | 1.42 | 1.29 | 1.14 | 0.94 | 0.69 | 0.34 | 0.09 | 0.00 | 0.00 | 0.00 |

| Estonia | 1.83 | 1.70 | 1.53 | 1.32 | 1.05 | 0.67 | 0.30 | 0.00 | 0.00 | 0.00 |

| Slovakia | 2.05 | 1.91 | 1.74 | 1.52 | 1.23 | 0.83 | 0.40 | 0.00 | 0.00 | 0.00 |

| Ireland | 2.38 | 2.25 | 2.09 | 1.88 | 1.61 | 1.24 | 0.68 | 0.30 | 0.00 | 0.00 |

| Latvia | 3.42 | 3.22 | 2.97 | 2.65 | 2.24 | 1.68 | 0.85 | 0.38 | 0.00 | 0.00 |

| Lithuania | 3.41 | 3.21 | 2.96 | 2.64 | 2.23 | 1.68 | 0.85 | 0.38 | 0.00 | 0.00 |

| Malta | 3.92 | 3.72 | 3.46 | 3.13 | 2.70 | 2.14 | 1.30 | 0.67 | 0.00 | 0.00 |

| Slovenia | 4.90 | 4.65 | 4.35 | 3.96 | 3.45 | 2.78 | 1.77 | 0.91 | 0.00 | 0.00 |

| Spain | 4.90 | 4.66 | 4.35 | 3.97 | 3.45 | 2.78 | 1.77 | 0.91 | 0.00 | 0.00 |

| Italy | 5.63 | 5.34 | 4.99 | 4.53 | 3.93 | 3.14 | 1.97 | 0.98 | 0.00 | 0.00 |

| Portugal | 8.97 | 8.52 | 7.95 | 7.23 | 6.26 | 5.16 | 3.62 | 1.59 | 0.80 | 0.00 |

| Cyprus | 13.58 | 12.75 | 11.70 | 10.35 | 8.56 | 6.90 | 5.06 | 1.99 | 1.28 | 0.00 |

| Greece | 34.16 | 31.80 | 28.85 | 25.06 | 20.01 | 14.47 | 11.92 | 7.67 | 3.24 | 2.16 |

| Pooled | 2.79 | |||||||||

| ESBies | 0.91 | 0.33 | 0.09 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| Subordination | 0% | 10% | 20% | 30% | 40% | 50% | 60% | 70% | 80% | 90% |

|---|---|---|---|---|---|---|---|---|---|---|

| Germany | 0.13 | 0.11 | 0.08 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| The Netherlands | 0.27 | 0.22 | 0.15 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Luxembourg | 0.27 | 0.22 | 0.15 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Austria | 0.50 | 0.42 | 0.32 | 0.19 | 0.06 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Finland | 0.50 | 0.42 | 0.32 | 0.19 | 0.06 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| France | 1.09 | 0.99 | 0.86 | 0.70 | 0.49 | 0.23 | 0.00 | 0.00 | 0.00 | 0.00 |

| Belgium | 1.42 | 1.29 | 1.14 | 0.94 | 0.69 | 0.34 | 0.09 | 0.00 | 0.00 | 0.00 |

| Estonia | 1.83 | 1.70 | 1.53 | 1.32 | 1.05 | 0.67 | 0.30 | 0.00 | 0.00 | 0.00 |

| Slovakia | 2.05 | 1.91 | 1.74 | 1.52 | 1.23 | 0.83 | 0.40 | 0.00 | 0.00 | 0.00 |

| Ireland | 2.38 | 2.25 | 2.09 | 1.88 | 1.61 | 1.24 | 0.68 | 0.30 | 0.00 | 0.00 |

| Latvia | 3.42 | 3.22 | 2.97 | 2.65 | 2.24 | 1.68 | 0.85 | 0.38 | 0.00 | 0.00 |

| Lithuania | 3.41 | 3.21 | 2.96 | 2.64 | 2.23 | 1.68 | 0.85 | 0.38 | 0.00 | 0.00 |

| Malta | 3.92 | 3.72 | 3.46 | 3.13 | 2.70 | 2.14 | 1.30 | 0.67 | 0.00 | 0.00 |

| Slovenia | 4.90 | 4.65 | 4.35 | 3.96 | 3.45 | 2.78 | 1.77 | 0.91 | 0.00 | 0.00 |

| Spain | 4.90 | 4.66 | 4.35 | 3.97 | 3.45 | 2.78 | 1.77 | 0.91 | 0.00 | 0.00 |

| Italy | 5.63 | 5.34 | 4.99 | 4.53 | 3.93 | 3.14 | 1.97 | 0.98 | 0.00 | 0.00 |

| Portugal | 8.97 | 8.52 | 7.95 | 7.23 | 6.26 | 5.16 | 3.62 | 1.59 | 0.80 | 0.00 |

| Cyprus | 13.58 | 12.75 | 11.70 | 10.35 | 8.56 | 6.90 | 5.06 | 1.99 | 1.28 | 0.00 |

| Greece | 34.16 | 31.80 | 28.85 | 25.06 | 20.01 | 14.47 | 11.92 | 7.67 | 3.24 | 2.16 |

| Pooled | 2.79 | |||||||||

| ESBies | 0.91 | 0.33 | 0.09 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

Notes: Table shows the senior bonds’ five-year expected loss rates (in percentage) in the benchmark calibration described in Subsection 4.3. It corresponds to the summary data presented in Figures 5 and 6. The first row of the table refers to the subordination level, which defines the size of the junior bond. The 0% subordination refers to the special case of no tranching. The remaining rows refer to the bonds of nation-states and, in the penultimate row, the GDP-weighted securitization of the 19 euro area sovereign bonds (without tranching), and in the final row ESBies (i.e. the senior tranche of the pooled security). Numbers in black denote five-year expected loss rates below 0.5%, which is the threshold below which we deem bonds to be safe, while numbers in grey denote loss rates above this safety threshold.

Senior bonds’ five-year expected loss rates in the benchmark calibration (%)

| Subordination | 0% | 10% | 20% | 30% | 40% | 50% | 60% | 70% | 80% | 90% |

|---|---|---|---|---|---|---|---|---|---|---|

| Germany | 0.13 | 0.11 | 0.08 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| The Netherlands | 0.27 | 0.22 | 0.15 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Luxembourg | 0.27 | 0.22 | 0.15 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Austria | 0.50 | 0.42 | 0.32 | 0.19 | 0.06 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Finland | 0.50 | 0.42 | 0.32 | 0.19 | 0.06 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| France | 1.09 | 0.99 | 0.86 | 0.70 | 0.49 | 0.23 | 0.00 | 0.00 | 0.00 | 0.00 |

| Belgium | 1.42 | 1.29 | 1.14 | 0.94 | 0.69 | 0.34 | 0.09 | 0.00 | 0.00 | 0.00 |

| Estonia | 1.83 | 1.70 | 1.53 | 1.32 | 1.05 | 0.67 | 0.30 | 0.00 | 0.00 | 0.00 |

| Slovakia | 2.05 | 1.91 | 1.74 | 1.52 | 1.23 | 0.83 | 0.40 | 0.00 | 0.00 | 0.00 |

| Ireland | 2.38 | 2.25 | 2.09 | 1.88 | 1.61 | 1.24 | 0.68 | 0.30 | 0.00 | 0.00 |

| Latvia | 3.42 | 3.22 | 2.97 | 2.65 | 2.24 | 1.68 | 0.85 | 0.38 | 0.00 | 0.00 |

| Lithuania | 3.41 | 3.21 | 2.96 | 2.64 | 2.23 | 1.68 | 0.85 | 0.38 | 0.00 | 0.00 |

| Malta | 3.92 | 3.72 | 3.46 | 3.13 | 2.70 | 2.14 | 1.30 | 0.67 | 0.00 | 0.00 |

| Slovenia | 4.90 | 4.65 | 4.35 | 3.96 | 3.45 | 2.78 | 1.77 | 0.91 | 0.00 | 0.00 |

| Spain | 4.90 | 4.66 | 4.35 | 3.97 | 3.45 | 2.78 | 1.77 | 0.91 | 0.00 | 0.00 |

| Italy | 5.63 | 5.34 | 4.99 | 4.53 | 3.93 | 3.14 | 1.97 | 0.98 | 0.00 | 0.00 |

| Portugal | 8.97 | 8.52 | 7.95 | 7.23 | 6.26 | 5.16 | 3.62 | 1.59 | 0.80 | 0.00 |

| Cyprus | 13.58 | 12.75 | 11.70 | 10.35 | 8.56 | 6.90 | 5.06 | 1.99 | 1.28 | 0.00 |

| Greece | 34.16 | 31.80 | 28.85 | 25.06 | 20.01 | 14.47 | 11.92 | 7.67 | 3.24 | 2.16 |

| Pooled | 2.79 | |||||||||

| ESBies | 0.91 | 0.33 | 0.09 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| Subordination | 0% | 10% | 20% | 30% | 40% | 50% | 60% | 70% | 80% | 90% |

|---|---|---|---|---|---|---|---|---|---|---|

| Germany | 0.13 | 0.11 | 0.08 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| The Netherlands | 0.27 | 0.22 | 0.15 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Luxembourg | 0.27 | 0.22 | 0.15 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Austria | 0.50 | 0.42 | 0.32 | 0.19 | 0.06 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Finland | 0.50 | 0.42 | 0.32 | 0.19 | 0.06 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| France | 1.09 | 0.99 | 0.86 | 0.70 | 0.49 | 0.23 | 0.00 | 0.00 | 0.00 | 0.00 |

| Belgium | 1.42 | 1.29 | 1.14 | 0.94 | 0.69 | 0.34 | 0.09 | 0.00 | 0.00 | 0.00 |

| Estonia | 1.83 | 1.70 | 1.53 | 1.32 | 1.05 | 0.67 | 0.30 | 0.00 | 0.00 | 0.00 |

| Slovakia | 2.05 | 1.91 | 1.74 | 1.52 | 1.23 | 0.83 | 0.40 | 0.00 | 0.00 | 0.00 |

| Ireland | 2.38 | 2.25 | 2.09 | 1.88 | 1.61 | 1.24 | 0.68 | 0.30 | 0.00 | 0.00 |

| Latvia | 3.42 | 3.22 | 2.97 | 2.65 | 2.24 | 1.68 | 0.85 | 0.38 | 0.00 | 0.00 |

| Lithuania | 3.41 | 3.21 | 2.96 | 2.64 | 2.23 | 1.68 | 0.85 | 0.38 | 0.00 | 0.00 |

| Malta | 3.92 | 3.72 | 3.46 | 3.13 | 2.70 | 2.14 | 1.30 | 0.67 | 0.00 | 0.00 |

| Slovenia | 4.90 | 4.65 | 4.35 | 3.96 | 3.45 | 2.78 | 1.77 | 0.91 | 0.00 | 0.00 |

| Spain | 4.90 | 4.66 | 4.35 | 3.97 | 3.45 | 2.78 | 1.77 | 0.91 | 0.00 | 0.00 |

| Italy | 5.63 | 5.34 | 4.99 | 4.53 | 3.93 | 3.14 | 1.97 | 0.98 | 0.00 | 0.00 |

| Portugal | 8.97 | 8.52 | 7.95 | 7.23 | 6.26 | 5.16 | 3.62 | 1.59 | 0.80 | 0.00 |

| Cyprus | 13.58 | 12.75 | 11.70 | 10.35 | 8.56 | 6.90 | 5.06 | 1.99 | 1.28 | 0.00 |

| Greece | 34.16 | 31.80 | 28.85 | 25.06 | 20.01 | 14.47 | 11.92 | 7.67 | 3.24 | 2.16 |

| Pooled | 2.79 | |||||||||

| ESBies | 0.91 | 0.33 | 0.09 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

Notes: Table shows the senior bonds’ five-year expected loss rates (in percentage) in the benchmark calibration described in Subsection 4.3. It corresponds to the summary data presented in Figures 5 and 6. The first row of the table refers to the subordination level, which defines the size of the junior bond. The 0% subordination refers to the special case of no tranching. The remaining rows refer to the bonds of nation-states and, in the penultimate row, the GDP-weighted securitization of the 19 euro area sovereign bonds (without tranching), and in the final row ESBies (i.e. the senior tranche of the pooled security). Numbers in black denote five-year expected loss rates below 0.5%, which is the threshold below which we deem bonds to be safe, while numbers in grey denote loss rates above this safety threshold.

The subordination level is, therefore, a key policy variable: it affects the senior bond’s safety and the volume of safe assets that is generated. Our simulations point to 30% as a reasonable middle ground between minimizing expected loss rates and maximizing safe asset supply: at this level, ESBies are slightly safer than the untranched German bund, and – as we shall see in the next subsection – the safe asset multiplier is a healthy 1.74.

4.3.2. Supply of safe assets

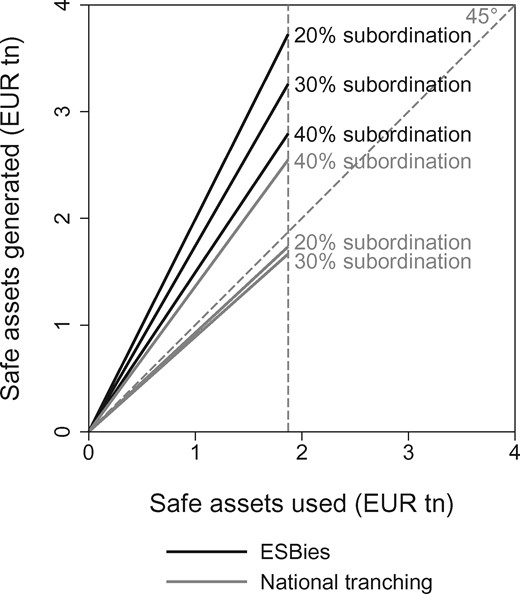

Supply of safe assets

Notes: Figure plots the volume of safe assets used in the securitization (horizontal axis) against those generated by the securitization (vertical axis). The solid lines refer to fixed subordination levels of ; those in black refer to ESBies, while the solid grey lines refer to tranched national bonds. Solid lines above the 45° line imply net generation of safe assets; lines below it imply net destruction of safe assets. The dashed vertical grey line intercepts the horizontal axis at €1.9tn, which represents the total outstanding face value of safe central government debt securities in 2015.

In our base case of 30% subordination, ESBies have an internal multiplier of 1.74. This contrasts with national tranching, which can cause a net destruction of safe assets because the subordinated component of safe nation-states’ debt may be rendered unsafe. Only at 40% subordination does the senior bond of an additional nation-state (namely France) become safe. This explains the non-monotonicity of the multiplier as a function of the uniform subordination level.

To prevent the net destruction of safe assets by tranching already safe nation-states’ debt, one could ‘optimize’ national tranching by minimizing the subordination level per country, such that each nation-state’s senior bond has an expected loss rate just below the 0.5% threshold. For Germany, this minimum is 0%; for France, 40%; and for Italy, 77%. Overall, optimized national tranching generates a multiplier of 1.75, similar to that of ESBies with 30% subordination. The design of ESBies, however, could also be optimized so that its expected loss rate is just below 0.5%: this occurs at a subordination level of 16%, at which ESBies have an internal multiplier of 2.1 – significantly higher than that under optimal national tranching. Moreover, ESBies are more robust to parameter uncertainty than nationally tranched bonds, since for the latter a smaller-than-expected recovery from a default would result in a haircut for the supposedly safe senior bond.

4.3.3. The attractiveness of EJBies

One might worry that the safety of ESBies comes at the expense of very risky EJBies that no investor would want to buy. This worry is fundamentally misguided: if investors hold sovereign bonds, then they will also hold synthetic securities backed by these bonds.

In fact, EJBies will be attractive to investors seeking to leverage their exposure to sovereign risk more cheaply than by using on-balance sheet leverage. This is because the first-loss piece comes with embedded leverage, the advantage of which can be illustrated with a simple example. Take the case of a hedge fund seeking exposure to a diversified portfolio of sovereign bonds. Imagine that the hedge fund wishes to enhance its return using leverage. It has two options. It could buy a pool of sovereign bonds on margin; the prime broker would set the cost of this margin funding at the interest rate of the hedge fund’s external funding. Alternatively, the hedge fund could buy EJBies, in which leverage is already embedded. In this case, the leverage is implicitly financed at the safe interest rate of ESBies, rather than at the hedge fund’s marginal rate of external funding, which is likely to be much higher. The hedge fund can, therefore, lever its portfolio more cheaply by using the leverage embedded in EJBies.

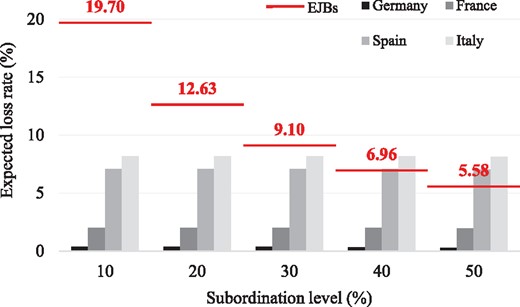

Junior bonds’ five-year expected loss rates by subordination level

Notes: Figure shows the expected loss rates of the junior tranche of national sovereign bonds versus that of the pooled euro area security. The data presented in this figure correspond to those reported in Table 4.

Junior bonds’ five-year expected loss rates in the benchmark calibration (%)

| Subordination | 10% | 20% | 30% | 40% | 50% | 60% | 70% | 80% | 90% | |

|---|---|---|---|---|---|---|---|---|---|---|

| Germany | 0.36 | 0.36 | 0.36 | 0.34 | 0.27 | 0.22 | 0.19 | 0.17 | 0.15 | |

| The Netherlands | 0.73 | 0.73 | 0.73 | 0.67 | 0.54 | 0.45 | 0.38 | 0.34 | 0.30 | |

| Luxembourg | 0.72 | 0.72 | 0.72 | 0.67 | 0.54 | 0.45 | 0.38 | 0.33 | 0.30 | |

| Austria | 1.22 | 1.22 | 1.22 | 1.17 | 1.00 | 0.84 | 0.72 | 0.63 | 0.56 | |

| Finland | 1.22 | 1.22 | 1.22 | 1.17 | 1.00 | 0.84 | 0.72 | 0.63 | 0.56 | |

| France | 1.99 | 1.99 | 1.99 | 1.98 | 1.94 | 1.81 | 1.55 | 1.36 | 1.21 | |

| Belgium | 2.52 | 2.52 | 2.52 | 2.50 | 2.49 | 2.30 | 2.02 | 1.77 | 1.57 | |

| Estonia | 3.02 | 3.02 | 3.02 | 3.01 | 3.00 | 2.85 | 2.62 | 2.29 | 2.03 | |

| Slovakia | 3.29 | 3.29 | 3.29 | 3.29 | 3.27 | 3.16 | 2.93 | 2.57 | 2.28 | |

| Ireland | 3.53 | 3.53 | 3.53 | 3.53 | 3.51 | 3.50 | 3.26 | 2.97 | 2.64 | |

| Latvia | 5.21 | 5.21 | 5.21 | 5.19 | 5.16 | 5.13 | 4.72 | 4.28 | 3.80 | |

| Lithuania | 5.19 | 5.19 | 5.19 | 5.17 | 5.14 | 5.11 | 4.70 | 4.26 | 3.79 | |

| Malta | 5.76 | 5.76 | 5.76 | 5.75 | 5.70 | 5.66 | 5.31 | 4.90 | 4.36 | |

| Slovenia | 7.07 | 7.07 | 7.07 | 7.07 | 7.02 | 6.98 | 6.60 | 6.12 | 5.44 | |

| Spain | 7.07 | 7.07 | 7.07 | 7.07 | 7.02 | 6.98 | 6.61 | 6.12 | 5.44 | |

| Italy | 8.18 | 8.18 | 8.18 | 8.18 | 8.12 | 8.07 | 7.62 | 7.04 | 6.25 | |

| Portugal | 13.03 | 13.03 | 13.03 | 13.03 | 12.78 | 12.53 | 12.13 | 11.01 | 9.96 | |

| Cyprus | 21.11 | 21.11 | 21.11 | 21.11 | 20.26 | 19.26 | 18.55 | 16.66 | 15.09 | |

| Greece | 55.39 | 55.39 | 55.39 | 55.39 | 53.85 | 48.99 | 45.51 | 41.89 | 37.72 | |

| EJBies | 19.70 | 12.63 | 9.10 | 6.96 | 5.58 | 4.65 | 3.99 | 3.49 | 3.10 | |

| Subordination | 10% | 20% | 30% | 40% | 50% | 60% | 70% | 80% | 90% | |

|---|---|---|---|---|---|---|---|---|---|---|

| Germany | 0.36 | 0.36 | 0.36 | 0.34 | 0.27 | 0.22 | 0.19 | 0.17 | 0.15 | |

| The Netherlands | 0.73 | 0.73 | 0.73 | 0.67 | 0.54 | 0.45 | 0.38 | 0.34 | 0.30 | |

| Luxembourg | 0.72 | 0.72 | 0.72 | 0.67 | 0.54 | 0.45 | 0.38 | 0.33 | 0.30 | |

| Austria | 1.22 | 1.22 | 1.22 | 1.17 | 1.00 | 0.84 | 0.72 | 0.63 | 0.56 | |

| Finland | 1.22 | 1.22 | 1.22 | 1.17 | 1.00 | 0.84 | 0.72 | 0.63 | 0.56 | |

| France | 1.99 | 1.99 | 1.99 | 1.98 | 1.94 | 1.81 | 1.55 | 1.36 | 1.21 | |

| Belgium | 2.52 | 2.52 | 2.52 | 2.50 | 2.49 | 2.30 | 2.02 | 1.77 | 1.57 | |

| Estonia | 3.02 | 3.02 | 3.02 | 3.01 | 3.00 | 2.85 | 2.62 | 2.29 | 2.03 | |

| Slovakia | 3.29 | 3.29 | 3.29 | 3.29 | 3.27 | 3.16 | 2.93 | 2.57 | 2.28 | |

| Ireland | 3.53 | 3.53 | 3.53 | 3.53 | 3.51 | 3.50 | 3.26 | 2.97 | 2.64 | |

| Latvia | 5.21 | 5.21 | 5.21 | 5.19 | 5.16 | 5.13 | 4.72 | 4.28 | 3.80 | |

| Lithuania | 5.19 | 5.19 | 5.19 | 5.17 | 5.14 | 5.11 | 4.70 | 4.26 | 3.79 | |

| Malta | 5.76 | 5.76 | 5.76 | 5.75 | 5.70 | 5.66 | 5.31 | 4.90 | 4.36 | |

| Slovenia | 7.07 | 7.07 | 7.07 | 7.07 | 7.02 | 6.98 | 6.60 | 6.12 | 5.44 | |

| Spain | 7.07 | 7.07 | 7.07 | 7.07 | 7.02 | 6.98 | 6.61 | 6.12 | 5.44 | |

| Italy | 8.18 | 8.18 | 8.18 | 8.18 | 8.12 | 8.07 | 7.62 | 7.04 | 6.25 | |

| Portugal | 13.03 | 13.03 | 13.03 | 13.03 | 12.78 | 12.53 | 12.13 | 11.01 | 9.96 | |

| Cyprus | 21.11 | 21.11 | 21.11 | 21.11 | 20.26 | 19.26 | 18.55 | 16.66 | 15.09 | |

| Greece | 55.39 | 55.39 | 55.39 | 55.39 | 53.85 | 48.99 | 45.51 | 41.89 | 37.72 | |

| EJBies | 19.70 | 12.63 | 9.10 | 6.96 | 5.58 | 4.65 | 3.99 | 3.49 | 3.10 | |

Notes: Table shows the junior bonds’ five-year expected loss rates (in percentage) in the benchmark calibration described in Subsection 4.3. It corresponds to the summary data presented in Figure 8. The first row of the table refers to the subordination level, which defines the size of the junior bond. The remaining rows refer to the bonds of nation-states and, in the final row, EJBies (i.e. the junior tranche of the pooled security). Numbers in black denote five-year expected loss rates below 7%, which represents the approximate threshold below which bonds would be rated investment grade, while numbers in grey denote expected loss rates above this threshold.

Junior bonds’ five-year expected loss rates in the benchmark calibration (%)

| Subordination | 10% | 20% | 30% | 40% | 50% | 60% | 70% | 80% | 90% | |

|---|---|---|---|---|---|---|---|---|---|---|

| Germany | 0.36 | 0.36 | 0.36 | 0.34 | 0.27 | 0.22 | 0.19 | 0.17 | 0.15 | |

| The Netherlands | 0.73 | 0.73 | 0.73 | 0.67 | 0.54 | 0.45 | 0.38 | 0.34 | 0.30 | |

| Luxembourg | 0.72 | 0.72 | 0.72 | 0.67 | 0.54 | 0.45 | 0.38 | 0.33 | 0.30 | |

| Austria | 1.22 | 1.22 | 1.22 | 1.17 | 1.00 | 0.84 | 0.72 | 0.63 | 0.56 | |

| Finland | 1.22 | 1.22 | 1.22 | 1.17 | 1.00 | 0.84 | 0.72 | 0.63 | 0.56 | |

| France | 1.99 | 1.99 | 1.99 | 1.98 | 1.94 | 1.81 | 1.55 | 1.36 | 1.21 | |

| Belgium | 2.52 | 2.52 | 2.52 | 2.50 | 2.49 | 2.30 | 2.02 | 1.77 | 1.57 | |

| Estonia | 3.02 | 3.02 | 3.02 | 3.01 | 3.00 | 2.85 | 2.62 | 2.29 | 2.03 | |

| Slovakia | 3.29 | 3.29 | 3.29 | 3.29 | 3.27 | 3.16 | 2.93 | 2.57 | 2.28 | |

| Ireland | 3.53 | 3.53 | 3.53 | 3.53 | 3.51 | 3.50 | 3.26 | 2.97 | 2.64 | |

| Latvia | 5.21 | 5.21 | 5.21 | 5.19 | 5.16 | 5.13 | 4.72 | 4.28 | 3.80 | |

| Lithuania | 5.19 | 5.19 | 5.19 | 5.17 | 5.14 | 5.11 | 4.70 | 4.26 | 3.79 | |

| Malta | 5.76 | 5.76 | 5.76 | 5.75 | 5.70 | 5.66 | 5.31 | 4.90 | 4.36 | |

| Slovenia | 7.07 | 7.07 | 7.07 | 7.07 | 7.02 | 6.98 | 6.60 | 6.12 | 5.44 | |

| Spain | 7.07 | 7.07 | 7.07 | 7.07 | 7.02 | 6.98 | 6.61 | 6.12 | 5.44 | |

| Italy | 8.18 | 8.18 | 8.18 | 8.18 | 8.12 | 8.07 | 7.62 | 7.04 | 6.25 | |

| Portugal | 13.03 | 13.03 | 13.03 | 13.03 | 12.78 | 12.53 | 12.13 | 11.01 | 9.96 | |

| Cyprus | 21.11 | 21.11 | 21.11 | 21.11 | 20.26 | 19.26 | 18.55 | 16.66 | 15.09 | |

| Greece | 55.39 | 55.39 | 55.39 | 55.39 | 53.85 | 48.99 | 45.51 | 41.89 | 37.72 | |

| EJBies | 19.70 | 12.63 | 9.10 | 6.96 | 5.58 | 4.65 | 3.99 | 3.49 | 3.10 | |

| Subordination | 10% | 20% | 30% | 40% | 50% | 60% | 70% | 80% | 90% | |

|---|---|---|---|---|---|---|---|---|---|---|

| Germany | 0.36 | 0.36 | 0.36 | 0.34 | 0.27 | 0.22 | 0.19 | 0.17 | 0.15 | |

| The Netherlands | 0.73 | 0.73 | 0.73 | 0.67 | 0.54 | 0.45 | 0.38 | 0.34 | 0.30 | |

| Luxembourg | 0.72 | 0.72 | 0.72 | 0.67 | 0.54 | 0.45 | 0.38 | 0.33 | 0.30 | |

| Austria | 1.22 | 1.22 | 1.22 | 1.17 | 1.00 | 0.84 | 0.72 | 0.63 | 0.56 | |

| Finland | 1.22 | 1.22 | 1.22 | 1.17 | 1.00 | 0.84 | 0.72 | 0.63 | 0.56 | |

| France | 1.99 | 1.99 | 1.99 | 1.98 | 1.94 | 1.81 | 1.55 | 1.36 | 1.21 | |

| Belgium | 2.52 | 2.52 | 2.52 | 2.50 | 2.49 | 2.30 | 2.02 | 1.77 | 1.57 | |

| Estonia | 3.02 | 3.02 | 3.02 | 3.01 | 3.00 | 2.85 | 2.62 | 2.29 | 2.03 | |

| Slovakia | 3.29 | 3.29 | 3.29 | 3.29 | 3.27 | 3.16 | 2.93 | 2.57 | 2.28 | |

| Ireland | 3.53 | 3.53 | 3.53 | 3.53 | 3.51 | 3.50 | 3.26 | 2.97 | 2.64 | |

| Latvia | 5.21 | 5.21 | 5.21 | 5.19 | 5.16 | 5.13 | 4.72 | 4.28 | 3.80 | |

| Lithuania | 5.19 | 5.19 | 5.19 | 5.17 | 5.14 | 5.11 | 4.70 | 4.26 | 3.79 | |

| Malta | 5.76 | 5.76 | 5.76 | 5.75 | 5.70 | 5.66 | 5.31 | 4.90 | 4.36 | |

| Slovenia | 7.07 | 7.07 | 7.07 | 7.07 | 7.02 | 6.98 | 6.60 | 6.12 | 5.44 | |

| Spain | 7.07 | 7.07 | 7.07 | 7.07 | 7.02 | 6.98 | 6.61 | 6.12 | 5.44 | |

| Italy | 8.18 | 8.18 | 8.18 | 8.18 | 8.12 | 8.07 | 7.62 | 7.04 | 6.25 | |

| Portugal | 13.03 | 13.03 | 13.03 | 13.03 | 12.78 | 12.53 | 12.13 | 11.01 | 9.96 | |

| Cyprus | 21.11 | 21.11 | 21.11 | 21.11 | 20.26 | 19.26 | 18.55 | 16.66 | 15.09 | |

| Greece | 55.39 | 55.39 | 55.39 | 55.39 | 53.85 | 48.99 | 45.51 | 41.89 | 37.72 | |

| EJBies | 19.70 | 12.63 | 9.10 | 6.96 | 5.58 | 4.65 | 3.99 | 3.49 | 3.10 | |

Notes: Table shows the junior bonds’ five-year expected loss rates (in percentage) in the benchmark calibration described in Subsection 4.3. It corresponds to the summary data presented in Figure 8. The first row of the table refers to the subordination level, which defines the size of the junior bond. The remaining rows refer to the bonds of nation-states and, in the final row, EJBies (i.e. the junior tranche of the pooled security). Numbers in black denote five-year expected loss rates below 7%, which represents the approximate threshold below which bonds would be rated investment grade, while numbers in grey denote expected loss rates above this threshold.

One might wonder whether markets have sufficient capacity to absorb a large quantity of EJBies with risk characteristics similar to those of the four lowest-rated euro area nation-states. With an underlying portfolio of €1tn, for example, EJBies with 30% subordination would have a face value of €0.3tn. At the same time, they would supplant €0.21tn of Italian, Portuguese, Cypriot and Greek debt, and an additional €0.11tn of Spanish debt, so that the overall supply of such moderately risky securities would not change much. Moreover, a hypothetical €0.3tn market for EJBies should be compared with the global high-yield market: non-euro area nation-states rated BB or BBB had outstanding debt of €4.1tn in 2012. EJBies would appeal to investors in such high-yield securities, as they would deliver high expected returns owing to their embedded leverage.

4.3.4. Sub-tranching EJBies to cater to different investors

In principle, the EJB component could be sub-tranched or repackaged in ways that make them more desirable to investors with different risk appetites. For instance, it is possible to sub-tranche the junior bond into a first-loss ‘equity’ piece and a mezzanine bond, each catering to a different clientele, as envisaged by Corsetti et al. (2016). Risk-averse investors, such as insurance companies and pension funds, would be attracted to the mezzanine bond; others specialized in high-yield debt, such as hedge funds, would prefer the first-loss piece.

We consider three sub-tranching types: a 50/50 split, whereby the equity piece comprises 15%, and the mezzanine bond 15%, of the underlying face value; a two-thirds/one-third split, whereby the equity piece comprises 20% and the mezzanine bond 10%; and a third case in which the equity piece comprises 25% and the mezzanine bond 5%.

With the 50/50 split, the mezzanine bond has an expected loss rate of 2.68%. This is slightly lower than that of Latvian sovereign bonds and slightly higher than Irish sovereign bonds, and maps to a credit rating of approximately A (i.e. ranked 6 on a 1–22 rating scale), which is firmly investment grade. The equity piece has an expected loss rate of 15.52%, which is slightly higher than that of Cypriot sovereign bonds, and would be assigned a credit rating of B+ (i.e. ranked 14 on a 1–22 rating scale), making it a ‘speculative’ high-yield security.

As the size of the equity piece increases, such that the mezzanine bond is protected by a larger first-loss piece, the expected loss rate of the mezzanine bond falls. With a 10% mezzanine bond and a 20% equity piece, the expected loss rate of the mezzanine falls to 2.40%, which is similar to that of Irish sovereign bonds and maps to a credit rating of approximately A+ (i.e. ranked 5 on a 1–22 rating scale). With a 5% mezzanine bond and a 25% equity piece, the expected loss rate of the mezzanine falls to 1.54%, which is similar to that of Belgian bonds and maps to a rating of AA (i.e. ranked 3 on a 1–22 rating scale).

Similarly, the expected loss rate of the equity piece decreases as its size increases, since the same quantum of losses is spread over a larger tranche. With a 5%/25% split between mezzanine and equity, the equity piece has an expected loss rate of 10.61%, which is slightly below that of Portuguese sovereign bonds and below investment grade. At this level of riskiness, the equity piece would be an attractive investment proposition for hedge funds and other specialized investors in high-yield debt.

4.4. Adverse calibration of the numerical simulation

In the benchmark calibration of the simulation, commonality in defaults comes from credit ratings conditional on the aggregate state, namely whether the euro area economy is in the catastrophic state 1, bad state 2 or good state 3. To consider a more adverse calibration, we build in further cross-country dependence. This provides a pessimistic robustness check and allows us to evaluate how ESBies would perform in adverse conditions relative to other security designs. We make four additional contagion assumptions, imposed sequentially in the following order:

Whenever there is a German default, others default with 50% probability.

Whenever there is a French default, other nation-states default with 40% probability, except the five highest rated nation-states, which default with 10% probability.

Whenever there is an Italian default, the five highest rated nation-states default with 5% probability; the next three nation-states (France, Belgium and Estonia) default with 10% probability; and the other nation-states default with 40% probability – unless any of these nation-states had defaulted at step 1 or 2.

Whenever there is a Spanish default, the five highest rated nation-states default with 5% probability; the next three nation-states default with 10% probability; and the other nation-states default with 40% probability – unless any of these nation-states had defaulted at step 1, 2 or 3.6

These contagion assumptions substantially increase cross-country default correlations, as is evident in Panel B (relative to Panel A) of Table 2. The first principal component of defaults now explains 42% of covariation in default rates, compared with 29% in the benchmark calibration, and the first three principal components account for 64% of the covariation compared with 57% before. Table 5 shows the conditional default probabilities, which given the way we calibrated the adverse simulation have the feature that euro area nation-states are very sensitive to the default of Germany, France, Italy or Spain.

Conditional default probabilities (%)

| Benchmark calibration | Adverse calibration | |||||||

|---|---|---|---|---|---|---|---|---|

| conditional on a default by: | conditional on a default by: | |||||||

| Germany | France | Spain | Italy | Germany | France | Spain | Italy | |

| Germany | 100 | 3 | 2 | 2 | 100 | 18 | 12 | 11 |

| The Netherlands | 7 | 6 | 4 | 4 | 26 | 19 | 14 | 14 |

| Luxembourg | 7 | 6 | 4 | 4 | 25 | 20 | 14 | 14 |

| Austria | 10 | 9 | 7 | 7 | 28 | 22 | 16 | 16 |

| Finland | 10 | 9 | 7 | 7 | 28 | 22 | 16 | 16 |

| France | 17 | 100 | 11 | 11 | 46 | 100 | 28 | 27 |

| Belgium | 20 | 19 | 14 | 13 | 44 | 45 | 31 | 30 |

| Estonia | 24 | 22 | 16 | 16 | 46 | 47 | 32 | 32 |

| Slovakia | 24 | 23 | 17 | 16 | 70 | 69 | 62 | 61 |

| Ireland | 28 | 25 | 19 | 18 | 70 | 70 | 63 | 62 |

| Latvia | 35 | 33 | 25 | 24 | 72 | 72 | 65 | 64 |

| Lithuania | 35 | 33 | 25 | 24 | 72 | 72 | 65 | 64 |

| Malta | 39 | 36 | 28 | 27 | 73 | 73 | 66 | 65 |

| Slovenia | 44 | 41 | 32 | 31 | 75 | 74 | 68 | 67 |

| Spain | 43 | 40 | 100 | 31 | 81 | 77 | 100 | 67 |

| Italy | 47 | 44 | 35 | 100 | 84 | 79 | 72 | 100 |

| Portugal | 56 | 52 | 44 | 43 | 80 | 79 | 74 | 73 |

| Cyprus | 62 | 59 | 52 | 51 | 82 | 82 | 77 | 77 |

| Greece | 88 | 86 | 82 | 81 | 93 | 93 | 91 | 91 |

| Benchmark calibration | Adverse calibration | |||||||

|---|---|---|---|---|---|---|---|---|

| conditional on a default by: | conditional on a default by: | |||||||

| Germany | France | Spain | Italy | Germany | France | Spain | Italy | |

| Germany | 100 | 3 | 2 | 2 | 100 | 18 | 12 | 11 |

| The Netherlands | 7 | 6 | 4 | 4 | 26 | 19 | 14 | 14 |

| Luxembourg | 7 | 6 | 4 | 4 | 25 | 20 | 14 | 14 |

| Austria | 10 | 9 | 7 | 7 | 28 | 22 | 16 | 16 |

| Finland | 10 | 9 | 7 | 7 | 28 | 22 | 16 | 16 |

| France | 17 | 100 | 11 | 11 | 46 | 100 | 28 | 27 |

| Belgium | 20 | 19 | 14 | 13 | 44 | 45 | 31 | 30 |

| Estonia | 24 | 22 | 16 | 16 | 46 | 47 | 32 | 32 |

| Slovakia | 24 | 23 | 17 | 16 | 70 | 69 | 62 | 61 |

| Ireland | 28 | 25 | 19 | 18 | 70 | 70 | 63 | 62 |

| Latvia | 35 | 33 | 25 | 24 | 72 | 72 | 65 | 64 |

| Lithuania | 35 | 33 | 25 | 24 | 72 | 72 | 65 | 64 |

| Malta | 39 | 36 | 28 | 27 | 73 | 73 | 66 | 65 |

| Slovenia | 44 | 41 | 32 | 31 | 75 | 74 | 68 | 67 |

| Spain | 43 | 40 | 100 | 31 | 81 | 77 | 100 | 67 |

| Italy | 47 | 44 | 35 | 100 | 84 | 79 | 72 | 100 |

| Portugal | 56 | 52 | 44 | 43 | 80 | 79 | 74 | 73 |

| Cyprus | 62 | 59 | 52 | 51 | 82 | 82 | 77 | 77 |

| Greece | 88 | 86 | 82 | 81 | 93 | 93 | 91 | 91 |

Notes: Table shows the default probabilities of euro area nation-states (given in the rows of the table) conditional on the default of Germany, France, Spain or Italy (given in the columns). These conditional default probabilities are shown for the benchmark calibration (Subsection 4.3) and the adverse calibration (Subsection 4.4). In the benchmark calibration, correlations between nation-states’ default probabilities arise entirely out of the state of the euro area economy and similarity in credit ratings. Default probabilities are otherwise independent. Conditional default probabilities are shown for the benchmark calibration for comparison with those of the adverse calibration, in which there are four additional contagion assumptions governing the correlation matrix of default probabilities. Owing to these additional contagion assumptions, default probabilities conditional on the default of Germany, France, Spain or Italy increase monotonically in the adverse calibration relative to the benchmark calibration of the simulation model. If Italy defaults, for example, Spain then has a probability of default of 67% in the adverse calibration, up from 31% in the benchmark calibration. This underscores the severity of the adverse calibration of the simulation model.

Conditional default probabilities (%)

| Benchmark calibration | Adverse calibration | |||||||

|---|---|---|---|---|---|---|---|---|

| conditional on a default by: | conditional on a default by: | |||||||

| Germany | France | Spain | Italy | Germany | France | Spain | Italy | |

| Germany | 100 | 3 | 2 | 2 | 100 | 18 | 12 | 11 |

| The Netherlands | 7 | 6 | 4 | 4 | 26 | 19 | 14 | 14 |

| Luxembourg | 7 | 6 | 4 | 4 | 25 | 20 | 14 | 14 |

| Austria | 10 | 9 | 7 | 7 | 28 | 22 | 16 | 16 |

| Finland | 10 | 9 | 7 | 7 | 28 | 22 | 16 | 16 |

| France | 17 | 100 | 11 | 11 | 46 | 100 | 28 | 27 |

| Belgium | 20 | 19 | 14 | 13 | 44 | 45 | 31 | 30 |

| Estonia | 24 | 22 | 16 | 16 | 46 | 47 | 32 | 32 |

| Slovakia | 24 | 23 | 17 | 16 | 70 | 69 | 62 | 61 |

| Ireland | 28 | 25 | 19 | 18 | 70 | 70 | 63 | 62 |

| Latvia | 35 | 33 | 25 | 24 | 72 | 72 | 65 | 64 |

| Lithuania | 35 | 33 | 25 | 24 | 72 | 72 | 65 | 64 |

| Malta | 39 | 36 | 28 | 27 | 73 | 73 | 66 | 65 |

| Slovenia | 44 | 41 | 32 | 31 | 75 | 74 | 68 | 67 |

| Spain | 43 | 40 | 100 | 31 | 81 | 77 | 100 | 67 |

| Italy | 47 | 44 | 35 | 100 | 84 | 79 | 72 | 100 |

| Portugal | 56 | 52 | 44 | 43 | 80 | 79 | 74 | 73 |

| Cyprus | 62 | 59 | 52 | 51 | 82 | 82 | 77 | 77 |

| Greece | 88 | 86 | 82 | 81 | 93 | 93 | 91 | 91 |

| Benchmark calibration | Adverse calibration | |||||||

|---|---|---|---|---|---|---|---|---|

| conditional on a default by: | conditional on a default by: | |||||||

| Germany | France | Spain | Italy | Germany | France | Spain | Italy | |

| Germany | 100 | 3 | 2 | 2 | 100 | 18 | 12 | 11 |

| The Netherlands | 7 | 6 | 4 | 4 | 26 | 19 | 14 | 14 |

| Luxembourg | 7 | 6 | 4 | 4 | 25 | 20 | 14 | 14 |

| Austria | 10 | 9 | 7 | 7 | 28 | 22 | 16 | 16 |

| Finland | 10 | 9 | 7 | 7 | 28 | 22 | 16 | 16 |

| France | 17 | 100 | 11 | 11 | 46 | 100 | 28 | 27 |

| Belgium | 20 | 19 | 14 | 13 | 44 | 45 | 31 | 30 |

| Estonia | 24 | 22 | 16 | 16 | 46 | 47 | 32 | 32 |

| Slovakia | 24 | 23 | 17 | 16 | 70 | 69 | 62 | 61 |

| Ireland | 28 | 25 | 19 | 18 | 70 | 70 | 63 | 62 |

| Latvia | 35 | 33 | 25 | 24 | 72 | 72 | 65 | 64 |

| Lithuania | 35 | 33 | 25 | 24 | 72 | 72 | 65 | 64 |

| Malta | 39 | 36 | 28 | 27 | 73 | 73 | 66 | 65 |

| Slovenia | 44 | 41 | 32 | 31 | 75 | 74 | 68 | 67 |

| Spain | 43 | 40 | 100 | 31 | 81 | 77 | 100 | 67 |

| Italy | 47 | 44 | 35 | 100 | 84 | 79 | 72 | 100 |

| Portugal | 56 | 52 | 44 | 43 | 80 | 79 | 74 | 73 |

| Cyprus | 62 | 59 | 52 | 51 | 82 | 82 | 77 | 77 |

| Greece | 88 | 86 | 82 | 81 | 93 | 93 | 91 | 91 |

Notes: Table shows the default probabilities of euro area nation-states (given in the rows of the table) conditional on the default of Germany, France, Spain or Italy (given in the columns). These conditional default probabilities are shown for the benchmark calibration (Subsection 4.3) and the adverse calibration (Subsection 4.4). In the benchmark calibration, correlations between nation-states’ default probabilities arise entirely out of the state of the euro area economy and similarity in credit ratings. Default probabilities are otherwise independent. Conditional default probabilities are shown for the benchmark calibration for comparison with those of the adverse calibration, in which there are four additional contagion assumptions governing the correlation matrix of default probabilities. Owing to these additional contagion assumptions, default probabilities conditional on the default of Germany, France, Spain or Italy increase monotonically in the adverse calibration relative to the benchmark calibration of the simulation model. If Italy defaults, for example, Spain then has a probability of default of 67% in the adverse calibration, up from 31% in the benchmark calibration. This underscores the severity of the adverse calibration of the simulation model.

Five-year expected loss rates for status quo sovereign bonds are much higher than in the benchmark calibration (Table 6). Now, only untranched German sovereign bonds are safe, so that status quo safe asset supply is €1.1tn, compared with €1.9tn in the benchmark calibration. France’s expected loss rate increases from 1.09% in the benchmark to 1.94% in the adverse calibration; Spain’s from 4.90% to 6.80%; and Italy’s from 5.63% to 7.22%.

Five-year expected loss rates in the adverse calibration (%)

| Subordination | 0% | 10% | 20% | 30% | 40% | 50% | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Tranche | S | J | S | J | S | J | S | J | S | J | |

| Germany | 0.50 | 0.40 | 1.43 | 0.27 | 1.43 | 0.11 | 1.42 | 0.00 | 1.26 | 0.00 | 1.01 |

| The Netherlands | 0.69 | 0.55 | 1.94 | 0.38 | 1.94 | 0.16 | 1.93 | 0.00 | 1.73 | 0.00 | 1.38 |

| Luxembourg | 0.69 | 0.55 | 1.94 | 0.38 | 1.94 | 0.16 | 1.93 | 0.00 | 1.73 | 0.00 | 1.38 |

| Austria | 0.96 | 0.80 | 2.41 | 0.60 | 2.41 | 0.35 | 2.40 | 0.09 | 2.27 | 0.00 | 1.93 |

| Finland | 0.96 | 0.80 | 2.41 | 0.60 | 2.41 | 0.35 | 2.40 | 0.09 | 2.27 | 0.00 | 1.93 |

| France | 1.94 | 1.75 | 3.66 | 1.51 | 3.66 | 1.20 | 3.66 | 0.81 | 3.63 | 0.33 | 3.54 |

| Belgium | 2.64 | 2.40 | 4.80 | 2.10 | 4.80 | 1.71 | 4.80 | 1.22 | 4.76 | 0.54 | 4.74 |

| Estonia | 3.10 | 2.87 | 5.23 | 2.57 | 5.23 | 2.19 | 5.23 | 1.70 | 5.20 | 1.03 | 5.18 |

| Slovakia | 5.58 | 5.16 | 9.30 | 4.65 | 9.30 | 3.98 | 9.30 | 3.13 | 9.25 | 1.97 | 9.19 |

| Ireland | 6.05 | 5.68 | 9.40 | 5.21 | 9.40 | 4.62 | 9.40 | 3.83 | 9.37 | 2.80 | 9.30 |

| Latvia | 6.81 | 6.38 | 10.66 | 5.85 | 10.66 | 5.16 | 10.66 | 4.26 | 10.62 | 3.09 | 10.53 |

| Lithuania | 6.80 | 6.37 | 10.64 | 5.84 | 10.64 | 5.15 | 10.64 | 4.26 | 10.61 | 3.08 | 10.52 |

| Malta | 7.32 | 6.91 | 11.04 | 6.39 | 11.04 | 5.73 | 11.04 | 4.85 | 11.03 | 3.72 | 10.92 |

| Slovenia | 8.17 | 7.74 | 12.05 | 7.20 | 12.05 | 6.51 | 12.05 | 5.59 | 12.05 | 4.41 | 11.94 |

| Spain | 6.80 | 6.45 | 9.94 | 6.02 | 9.94 | 5.46 | 9.94 | 4.71 | 9.94 | 3.75 | 9.86 |

| Italy | 7.22 | 6.85 | 10.58 | 6.38 | 10.58 | 5.78 | 10.58 | 4.98 | 10.58 | 3.96 | 10.49 |

| Portugal | 11.80 | 11.21 | 17.12 | 10.47 | 17.12 | 9.52 | 17.12 | 8.25 | 17.12 | 6.78 | 16.82 |

| Cyprus | 16.07 | 15.12 | 24.61 | 13.93 | 24.61 | 12.41 | 24.61 | 10.37 | 24.61 | 8.41 | 23.73 |

| Greece | 35.19 | 32.79 | 56.77 | 29.79 | 56.77 | 25.94 | 56.77 | 20.80 | 56.77 | 15.15 | 55.23 |

| Pooled | 3.84 | ||||||||||

| ESBies/EJBies | 2.02 | 20.24 | 1.02 | 15.13 | 0.42 | 11.81 | 0.15 | 9.38 | 0.03 | 7.64 | |

| Subordination | 0% | 10% | 20% | 30% | 40% | 50% | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Tranche | S | J | S | J | S | J | S | J | S | J | |

| Germany | 0.50 | 0.40 | 1.43 | 0.27 | 1.43 | 0.11 | 1.42 | 0.00 | 1.26 | 0.00 | 1.01 |

| The Netherlands | 0.69 | 0.55 | 1.94 | 0.38 | 1.94 | 0.16 | 1.93 | 0.00 | 1.73 | 0.00 | 1.38 |

| Luxembourg | 0.69 | 0.55 | 1.94 | 0.38 | 1.94 | 0.16 | 1.93 | 0.00 | 1.73 | 0.00 | 1.38 |

| Austria | 0.96 | 0.80 | 2.41 | 0.60 | 2.41 | 0.35 | 2.40 | 0.09 | 2.27 | 0.00 | 1.93 |

| Finland | 0.96 | 0.80 | 2.41 | 0.60 | 2.41 | 0.35 | 2.40 | 0.09 | 2.27 | 0.00 | 1.93 |

| France | 1.94 | 1.75 | 3.66 | 1.51 | 3.66 | 1.20 | 3.66 | 0.81 | 3.63 | 0.33 | 3.54 |

| Belgium | 2.64 | 2.40 | 4.80 | 2.10 | 4.80 | 1.71 | 4.80 | 1.22 | 4.76 | 0.54 | 4.74 |

| Estonia | 3.10 | 2.87 | 5.23 | 2.57 | 5.23 | 2.19 | 5.23 | 1.70 | 5.20 | 1.03 | 5.18 |

| Slovakia | 5.58 | 5.16 | 9.30 | 4.65 | 9.30 | 3.98 | 9.30 | 3.13 | 9.25 | 1.97 | 9.19 |

| Ireland | 6.05 | 5.68 | 9.40 | 5.21 | 9.40 | 4.62 | 9.40 | 3.83 | 9.37 | 2.80 | 9.30 |

| Latvia | 6.81 | 6.38 | 10.66 | 5.85 | 10.66 | 5.16 | 10.66 | 4.26 | 10.62 | 3.09 | 10.53 |

| Lithuania | 6.80 | 6.37 | 10.64 | 5.84 | 10.64 | 5.15 | 10.64 | 4.26 | 10.61 | 3.08 | 10.52 |

| Malta | 7.32 | 6.91 | 11.04 | 6.39 | 11.04 | 5.73 | 11.04 | 4.85 | 11.03 | 3.72 | 10.92 |

| Slovenia | 8.17 | 7.74 | 12.05 | 7.20 | 12.05 | 6.51 | 12.05 | 5.59 | 12.05 | 4.41 | 11.94 |

| Spain | 6.80 | 6.45 | 9.94 | 6.02 | 9.94 | 5.46 | 9.94 | 4.71 | 9.94 | 3.75 | 9.86 |

| Italy | 7.22 | 6.85 | 10.58 | 6.38 | 10.58 | 5.78 | 10.58 | 4.98 | 10.58 | 3.96 | 10.49 |

| Portugal | 11.80 | 11.21 | 17.12 | 10.47 | 17.12 | 9.52 | 17.12 | 8.25 | 17.12 | 6.78 | 16.82 |

| Cyprus | 16.07 | 15.12 | 24.61 | 13.93 | 24.61 | 12.41 | 24.61 | 10.37 | 24.61 | 8.41 | 23.73 |

| Greece | 35.19 | 32.79 | 56.77 | 29.79 | 56.77 | 25.94 | 56.77 | 20.80 | 56.77 | 15.15 | 55.23 |

| Pooled | 3.84 | ||||||||||

| ESBies/EJBies | 2.02 | 20.24 | 1.02 | 15.13 | 0.42 | 11.81 | 0.15 | 9.38 | 0.03 | 7.64 | |

Notes: Table shows the five-year expected loss rates (in percentage) in the adverse calibration described in Subsection 4.4. The first row refers to the subordination level, which defines the size of the junior bond. The second row refers to the tranche type; ‘S’ (in black) denotes the senior bond and ‘J’ (in grey) the junior bond. The cell referring to 0% subordination is blank, since there is no tranching in this case: all bonds are pari passu. The remaining rows refer to the bonds of nation-states and, in the final row, the pooled security, which represents a GDP-weighted securitization of the 19 euro area nation-states’ sovereign bonds.

Five-year expected loss rates in the adverse calibration (%)

| Subordination | 0% | 10% | 20% | 30% | 40% | 50% | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Tranche | S | J | S | J | S | J | S | J | S | J | |

| Germany | 0.50 | 0.40 | 1.43 | 0.27 | 1.43 | 0.11 | 1.42 | 0.00 | 1.26 | 0.00 | 1.01 |

| The Netherlands | 0.69 | 0.55 | 1.94 | 0.38 | 1.94 | 0.16 | 1.93 | 0.00 | 1.73 | 0.00 | 1.38 |

| Luxembourg | 0.69 | 0.55 | 1.94 | 0.38 | 1.94 | 0.16 | 1.93 | 0.00 | 1.73 | 0.00 | 1.38 |

| Austria | 0.96 | 0.80 | 2.41 | 0.60 | 2.41 | 0.35 | 2.40 | 0.09 | 2.27 | 0.00 | 1.93 |

| Finland | 0.96 | 0.80 | 2.41 | 0.60 | 2.41 | 0.35 | 2.40 | 0.09 | 2.27 | 0.00 | 1.93 |

| France | 1.94 | 1.75 | 3.66 | 1.51 | 3.66 | 1.20 | 3.66 | 0.81 | 3.63 | 0.33 | 3.54 |

| Belgium | 2.64 | 2.40 | 4.80 | 2.10 | 4.80 | 1.71 | 4.80 | 1.22 | 4.76 | 0.54 | 4.74 |

| Estonia | 3.10 | 2.87 | 5.23 | 2.57 | 5.23 | 2.19 | 5.23 | 1.70 | 5.20 | 1.03 | 5.18 |

| Slovakia | 5.58 | 5.16 | 9.30 | 4.65 | 9.30 | 3.98 | 9.30 | 3.13 | 9.25 | 1.97 | 9.19 |

| Ireland | 6.05 | 5.68 | 9.40 | 5.21 | 9.40 | 4.62 | 9.40 | 3.83 | 9.37 | 2.80 | 9.30 |

| Latvia | 6.81 | 6.38 | 10.66 | 5.85 | 10.66 | 5.16 | 10.66 | 4.26 | 10.62 | 3.09 | 10.53 |

| Lithuania | 6.80 | 6.37 | 10.64 | 5.84 | 10.64 | 5.15 | 10.64 | 4.26 | 10.61 | 3.08 | 10.52 |

| Malta | 7.32 | 6.91 | 11.04 | 6.39 | 11.04 | 5.73 | 11.04 | 4.85 | 11.03 | 3.72 | 10.92 |

| Slovenia | 8.17 | 7.74 | 12.05 | 7.20 | 12.05 | 6.51 | 12.05 | 5.59 | 12.05 | 4.41 | 11.94 |

| Spain | 6.80 | 6.45 | 9.94 | 6.02 | 9.94 | 5.46 | 9.94 | 4.71 | 9.94 | 3.75 | 9.86 |

| Italy | 7.22 | 6.85 | 10.58 | 6.38 | 10.58 | 5.78 | 10.58 | 4.98 | 10.58 | 3.96 | 10.49 |

| Portugal | 11.80 | 11.21 | 17.12 | 10.47 | 17.12 | 9.52 | 17.12 | 8.25 | 17.12 | 6.78 | 16.82 |

| Cyprus | 16.07 | 15.12 | 24.61 | 13.93 | 24.61 | 12.41 | 24.61 | 10.37 | 24.61 | 8.41 | 23.73 |

| Greece | 35.19 | 32.79 | 56.77 | 29.79 | 56.77 | 25.94 | 56.77 | 20.80 | 56.77 | 15.15 | 55.23 |

| Pooled | 3.84 | ||||||||||

| ESBies/EJBies | 2.02 | 20.24 | 1.02 | 15.13 | 0.42 | 11.81 | 0.15 | 9.38 | 0.03 | 7.64 | |

| Subordination | 0% | 10% | 20% | 30% | 40% | 50% | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Tranche | S | J | S | J | S | J | S | J | S | J | |

| Germany | 0.50 | 0.40 | 1.43 | 0.27 | 1.43 | 0.11 | 1.42 | 0.00 | 1.26 | 0.00 | 1.01 |

| The Netherlands | 0.69 | 0.55 | 1.94 | 0.38 | 1.94 | 0.16 | 1.93 | 0.00 | 1.73 | 0.00 | 1.38 |

| Luxembourg | 0.69 | 0.55 | 1.94 | 0.38 | 1.94 | 0.16 | 1.93 | 0.00 | 1.73 | 0.00 | 1.38 |

| Austria | 0.96 | 0.80 | 2.41 | 0.60 | 2.41 | 0.35 | 2.40 | 0.09 | 2.27 | 0.00 | 1.93 |

| Finland | 0.96 | 0.80 | 2.41 | 0.60 | 2.41 | 0.35 | 2.40 | 0.09 | 2.27 | 0.00 | 1.93 |

| France | 1.94 | 1.75 | 3.66 | 1.51 | 3.66 | 1.20 | 3.66 | 0.81 | 3.63 | 0.33 | 3.54 |

| Belgium | 2.64 | 2.40 | 4.80 | 2.10 | 4.80 | 1.71 | 4.80 | 1.22 | 4.76 | 0.54 | 4.74 |

| Estonia | 3.10 | 2.87 | 5.23 | 2.57 | 5.23 | 2.19 | 5.23 | 1.70 | 5.20 | 1.03 | 5.18 |

| Slovakia | 5.58 | 5.16 | 9.30 | 4.65 | 9.30 | 3.98 | 9.30 | 3.13 | 9.25 | 1.97 | 9.19 |

| Ireland | 6.05 | 5.68 | 9.40 | 5.21 | 9.40 | 4.62 | 9.40 | 3.83 | 9.37 | 2.80 | 9.30 |

| Latvia | 6.81 | 6.38 | 10.66 | 5.85 | 10.66 | 5.16 | 10.66 | 4.26 | 10.62 | 3.09 | 10.53 |

| Lithuania | 6.80 | 6.37 | 10.64 | 5.84 | 10.64 | 5.15 | 10.64 | 4.26 | 10.61 | 3.08 | 10.52 |

| Malta | 7.32 | 6.91 | 11.04 | 6.39 | 11.04 | 5.73 | 11.04 | 4.85 | 11.03 | 3.72 | 10.92 |

| Slovenia | 8.17 | 7.74 | 12.05 | 7.20 | 12.05 | 6.51 | 12.05 | 5.59 | 12.05 | 4.41 | 11.94 |

| Spain | 6.80 | 6.45 | 9.94 | 6.02 | 9.94 | 5.46 | 9.94 | 4.71 | 9.94 | 3.75 | 9.86 |

| Italy | 7.22 | 6.85 | 10.58 | 6.38 | 10.58 | 5.78 | 10.58 | 4.98 | 10.58 | 3.96 | 10.49 |

| Portugal | 11.80 | 11.21 | 17.12 | 10.47 | 17.12 | 9.52 | 17.12 | 8.25 | 17.12 | 6.78 | 16.82 |

| Cyprus | 16.07 | 15.12 | 24.61 | 13.93 | 24.61 | 12.41 | 24.61 | 10.37 | 24.61 | 8.41 | 23.73 |