Abstract

This paper examines apparent fraud among securitized nonagency loans using three indicators: unreported second liens, owner occupancy misreporting, and appraisal overstatements. We find that around 48% of loans exhibited at least one indicator of misrepresentation. Surprisingly, misreporting is similar in both low and full documentation loans and is associated with a 51% higher likelihood of delinquency. Two-thirds of loans with unreported second liens had the same originator issuing both the first and second lien. Misrepresentations in MBS pools can explain substantial cross-sectional differences in future losses. Losses were predictable and initiating from apparent fraud by MBS underwriters and loan originators.

Received August 24, 2015; accepted September 11, 2015 by Editor Matthew Spiegel.

At the heart of the recent financial crisis was an extremely rapid deterioration in the value of nonagency mortgage-backed securities (MBS) and collateralized debt obligations (CDO), derived from MBS. To fully understand the crisis, one needs to thoroughly understand the nature and incentives of the collateral that later underpinned many types of structured products. Mortgage fraud is a subject of interest to the financial press. However, it is very difficult to determine if cases in the news, prosecuted cases, and/or settlements are rare events or indicative of widespread patterns, and who are the responsible parties. This paper fills these voids by examining the role that borrowers, appraisers, originators, and MBS underwriters may have played in three different types of mortgage misrepresentations and their effects on MBS losses.

A matching algorithm allows us to link large data sets of nonagency MBS loan data from 2002 to 2007 with county-level transaction information and perform loan monitoring along three dimensions. First, we examine the prevalence of loans recorded in MBS loan-level data as having only a first lien, yet when matched to county-level information show a second-lien loan issued together (on the same day) with the first-lien loan. Second, we examine cases in which loan-level MBS data indicate that a house is owner occupied, but county-level data show that the tax records are sent to a different, nonbusiness address. Third, we examine the extent to which appraisal values are overstated using an industry-leading automated valuation model (AVM) that provides a statistical valuation for a house at the time of loan origination.

We find that 13.4% of loans reported as having no second lien (10.2% of all loans) do have a second lien. Approximately 7.7% of loans marked as owner occupied (6.7% of all loans) may not be owner occupied. Further, 44.9% of homes have appraisals that are 5% higher than an industry-leading AVM. Even though we only examine three forms of potential misreporting, our overall frequency of misreporting across all three dimensions is 48.8%.1 Aggregate misreporting frequencies are similar for low and full documentation loans, suggesting that misreporting is not simply due to lack of information disclosure. We also find that loans with an unreported second lien, occupancy status misreporting, or appraisal overstatement indicator are 97%, 8%, and 34% more likely to become delinquent than loans with no misreporting indicator. The findings are robust to using a measure of direct default and to the inclusion of core-based statistical area (CBSA)-origination quarter fixed effects and many other loan-level controls, indicating that our results are not simply explained by geographic patterns or loan characteristics.

Next, we examine the role of borrowers, appraisers, originators, and MBS underwriters in misreporting. In more than two-thirds of the cases of unreported second liens, the same originator issued the first and second liens on the same day, indicating that originators were aware of the second lien. Loans with unreported second liens were originated with interest rates similar to those of first-lien loans with correctly reported second liens, further indicating that originators were seemingly aware of and accounted for the second-lien risk. We find that the fraction of unreported second liens jumps around securitization thresholds, which suggests that originators misreported second liens with the intention of ultimate loan securitization. We examine the possibility that loan originators accurately reported second-lien data to underwriters, who later omitted this information at issuance. However, in explaining unreported second liens, both originator and underwriter fixed effects are economically important.

Owner occupancy misreporting is not accompanied by a materially higher interest rate, indicating that originators may have been largely unaware of buyers' intended usage of the property. Loans with inflated appraisal values sold with some premium, indicating that loan originators viewed these loans as riskier. For the most part, owner occupancy and appraisal overstatement misreporting do not change around securitization thresholds or vary much across originators, indicating that these practices were not driven by securitization.

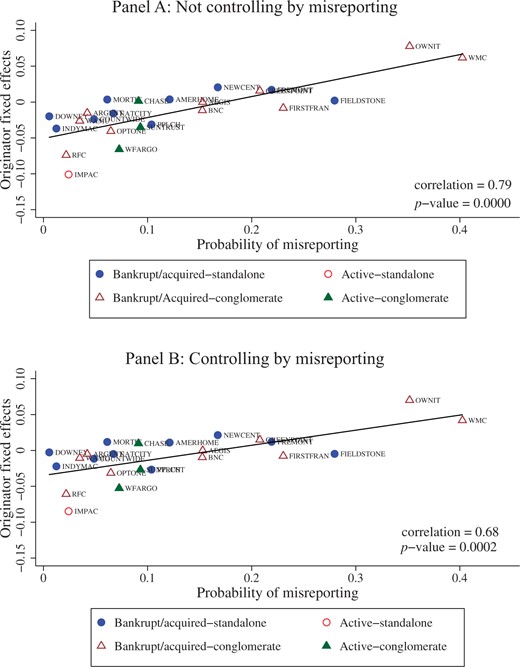

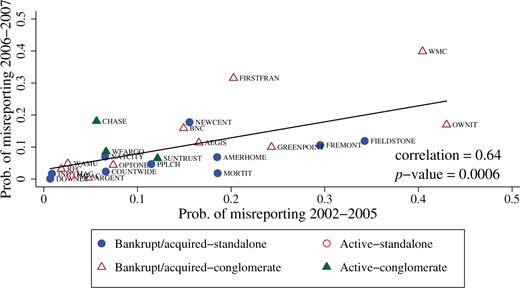

In contrast, second-lien misreporting varies considerably across originators, whether standalone or as part of a large corporation. Originators with high levels of second-lien misreporting also have abnormally poor loan performance even after controlling for the individual loan-level misrepresentation indicators. This suggests that our indicators are not capturing the full extent of fraud or some other aspect of origination practices that is correlated with mortgage misreporting. The prevalence of misreporting by originator and originator loan performance are fairly persistent over time. Second-lien misreporting increases from 2002 to 2005, primarily due to a gain in market share by originators that exhibited similarly high levels of second-lien misreporting even back in 2002. Second-lien misreporting plummets in early 2007 as originators with the highest levels of second-lien misreporting go out of business.

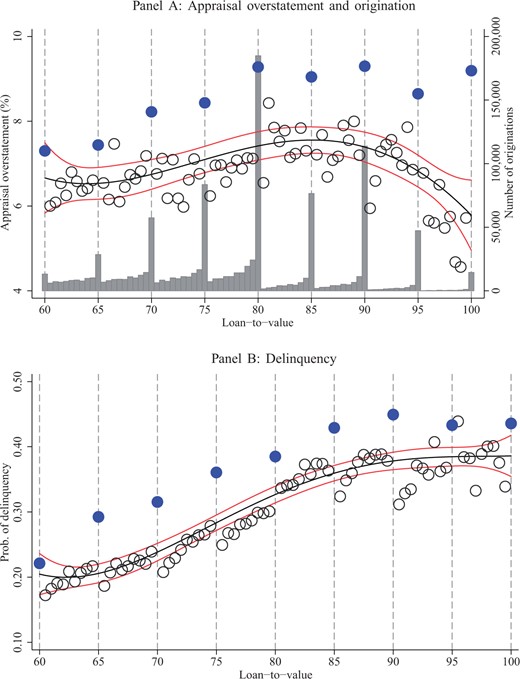

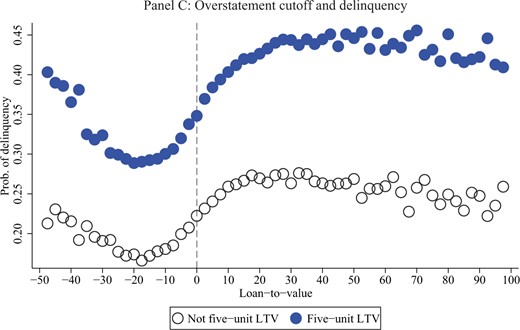

The strong relation between the appraisal indicator and future delinquency indicates that the AVM statistical model is substantially more accurate than most appraisers, but does not speak to whether the poor appraiser performance was due to random appraiser error or appraisers catering to loan officers. To examine these differences, we focus on refinances, where the value of the transaction is set purely by the appraisal. Appraisal overstatement is 74% more likely to occur on refinances than on purchases. Moreover, 49% of appraisals used for refinance cluster exactly on loan-to-value ratios in five-unit increments. This could be due to either appraisers targeting the amounts that loan officers wish to lend, or lenders setting loan amounts relative to the appraisals. Consistent with appraisers targeting numbers from loan officers, the clusters at round-number thresholds have consistently higher levels of appraisal overstatements and higher future delinquency rates as shown in panels A through C of Figure 4. The evidence demonstrates that appraisers largely target numbers from loan officers and that this leads to significantly higher future loan losses.

The evidence that loan originators were likely aware of second-lien misrepresentation raises the question of what bank underwriters knew. Monitoring services, such as Clayton Holdings, provided loan monitoring for a sample of loans for each individual MBS. These monitoring services list the three types of misreporting that we study, among others. This suggests that MBS underwriting banks knew that some of the MBS representations at issuance were incorrect. Thus, extremely poor MBS performance was not just a function of disclosure or bad luck; some information available before MBS issuance predicted their future demise.

Our paper adds to a growing literature examining mortgage misreporting that finds evidence typically for one measure in a particular county or bank (Ben-David 2011; Jiang, Nelson, and Vytlacil 2014; Garmaise 2015; Carrillo 2013).2 In a parallel study, Piskorski et al. (2015) use credit bureau data together with loan-level data from 2005 to 2007 to show that around 10% of nonagency loans exhibit owner occupancy and second-lien misreporting, which is later associated with a 60% higher probability of default, yet misreporting was not reflected in MBS pricing or subordination. The higher aggregate levels of misreporting that we find is explained by our inclusion of appraisal overstatements.3 It is comforting that although the papers use entirely different data sources, they reach similar conclusions concerning the existence of large-scale misreporting and its effects on loan performance. Piskorski et al. (2015) show that the effects of misreporting are not reflected in MBS pricing or subordination and yet misrepresentation is harmful to all rating classes, even senior tranches. Our combined inferences suggest that MBS investors were unaware of, yet adversely affected by, misrepresentation.

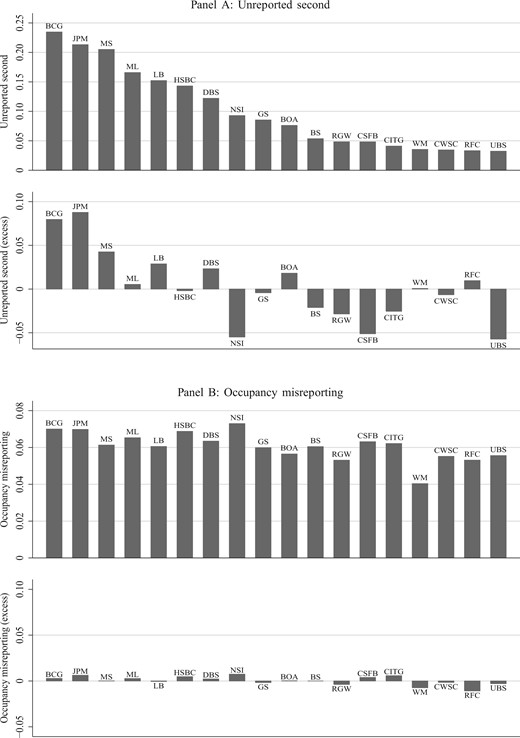

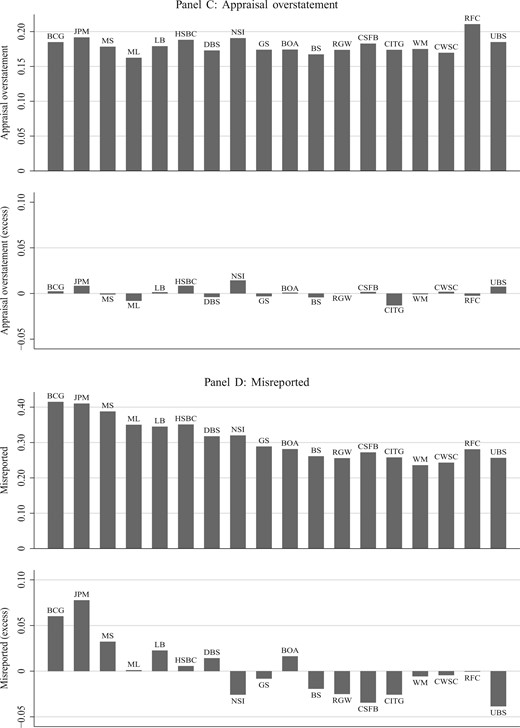

Drafts of our paper were posted online in April 2013 and pre-date any of the large Department of Justice (DOJ) settlements. Although all large banks in our sample also had large levels of apparent fraud, the ten banks with the most misreporting with our indicators are Barclays, JP Morgan, Morgan Stanley, Merrill Lynch, Lehman Brothers, HSBC, Deutsche Bank, Nomura Securities, Goldman Sachs, and Bank of America. Our findings provide detailed evidence that the large DOJ settlements with some of these banks are definitely justified and not an unjust shakedown as some pundits have suggested.4 They also suggest that more DOJ settlements should occur.

In addition to shedding light on the nonagency loan market, our paper is related to a large literature on problems in structured finance in the period prior to the recent crisis. Explanations for the extremely poor loan performance include a decrease in loan quality (Demyanyk and Van Hemert 2011) or a decrease in housing prices (Mayer, Pence, and Sherlund 2009), and poor incentives tied to the “originate-to-distribute” model (Keys et al. 2010; Purnanandam 2011; Keys, Seru, and Vig 2012). Our findings show that the loan-level problems were much greater than previously recognized. Ashcraft et al. (2010) show that residential mortgage-backed securities (RMBS) subordination standards deteriorated from 2005 to 2007. For CDOs, Griffin and Tang (2012) and Griffin et al. (2013) show that rating agencies issued inflated ratings, adjusted credit rating models upwards from 2004 to 2007, and sought to match their competitors' ratings to please issuers. Additionally, second liens, owner occupancy, and loan-to-value are key inputs in credit rating models, and rating agencies seemed to have accepted bank loan-level data as without verification. If investors were purchasing based on rating agency and investment bank certification, then there would be a strong incentive for underwriters to misreport. Together these findings suggest that there is considerable private information across deals and challenge the view that the crisis was a completely random event unrelated to structuring incentives. Following on this line of examination, in Griffin and Maturana (2016) analyze to what extent the fraud documented here caused differential patterns in house price inflation.

1. Mortgage Fraud, Data, and Measures

1.1 Mortgage fraud

Fraud refers to financial misrepresentation with the intent to deceive. The FBI distinguishes between two types of mortgage fraud: (1) fraud for property/housing, and (2) fraud for profit (Federal Bureau of Investigation 2011). The first type consists of misreporting by the borrower in order to obtain funding to purchase a primary property. The second type involves more sophisticated schemes to obtain illicit monetary gains from property sales. Methods to facilitate fraud include inflated appraisals, occupancy status misreporting, unreported second liens, property flipping, and falsification of the borrower's financial information, such as bank statements, tax return documents, income, assets, and liabilities. The three indicators of potential misrepresentation that we focus on are unreported second liens (often referred to as “silent seconds”), owner occupancy misreporting, and appraisal overstatements. We focus on these indicators because (1) they can be constructed on a large scale from available data, (2) they are commonly discussed forms of misrepresentation, and (3) they are used by firms in the loan monitoring industry (such as Clayton). We call these variables “indicators” because while they are constructed to identify loans associated with misrepresentation or fraud, they may capture loans that appear suspicious but have a legitimate justification.

Ultimately, whether a fraud indicator captures actual misrepresentation is an empirical question. In the first part of our analysis, we focus on misreporting without looking at which of the relevant parties are responsible. We then analyze the information that may have been known by buyers, appraisers, mortgage originators, and MBS underwriters. All of our indicators are constructed with information from public records on the closing date of the transaction, which means that in most cases, with the proper identifying information that were available to originators and underwriters, our indicators could have been constructed prior to MBS origination. Since the misreporting also has the profit-making motives of intent, and the facts suggest that the relevant parties had information to be sufficiently aware of the misreporting, fraud seems the more accurate, but less politically correct wording.

1.2 Data

The data for this study come from four main sources: Lewtan's ABSNet Loan and HomeVal data sets, along with DataQuick's Assessor and History files. The Lewtan data sets provide loan-level and home valuation information, and DataQuick provides house characteristic and transaction information. Lewtan is an industry leader in providing performance metrics and origination information on the mortgage loans that back U.S. nonagency MBS. Lewtan compiles and cleans loan-level information as reported in nonagency MBS raw servicer/trustee loan-level data tapes, like the one available in free writing prospectus documents. Lewtan's ABSNet Loan contains information about more than 18 million residential loans issued for the purchase or refinancing of properties between January 2002 and December 2011 and provides origination information, such as the appraised value of the property, the documentation provided by the borrower, the purpose of the property as reported by the borrower (owner occupied, second home, or investment), the loan amount, the loan-to-value ratio, the interest rate, the credit score of the borrower, and the origination date. Additionally, the database provides the payment history for each loan and other metrics. HomeVal, in contrast, provides home valuations at the time of origination based on Lewtan's ABSNet proprietary AVM. The AVM is developed by Collateral Analytics, a firm that specializes in AVM models and mortgage risk tools.5

DataQuick is one of the largest providers of real estate data in the United States. DataQuick's Assessor file holds detailed information on residential properties as registered from county assessors. In turn, the history file records more than 175 million transactions from January 2002 to December 2011, involving almost 62 million properties from the assessor file. The history file gives information on the transfer date of the property, the identities of the buyer and seller, the mailing address of the buyer, and the various loans involved in the transaction, among other information.

1.3 Merging process

The identity of the buyer and the property address are available in DataQuick, but not in ABSNet, which only provides the ZIP code. Since erroneous matching can lead to overstating misrepresented loans, we take a conservative approach and perform extensive diagnostics on our matching procedure.

Residential loans are matched with transactions according to their ZIP code, loan amount, interest rate type (fixed- or adjustable-rate mortgage), loan type (conventional, Federal Housing Administration (FHA), or veteran), originator, and purpose of transaction (refinance or purchase). Additionally, the transfer date is required to be within a [−15, 30]-day interval around the loan origination date, and the differences in transaction prices, when available, are required to be within $1,000. We only consider a transaction-loan pair a match when it is unique.

The algorithm matches 34.6% of the first liens with an initial loan amount over $30k in ABSNet. We compare characteristics between matched and unmatched loans and find that both samples are quite similar. In terms of geographic distribution, we obtain a higher matching rate in California and Florida, which are the most important states in our sample in terms of number of loan originations. These results, along with a detailed evaluation of the matching procedure and a description of the sample selection process, are available in the Internet Appendix.

1.4 Sample description

Table 1, panels A through C, provides a description of the main sample. After applying the filters above, we end with a sample of 3,143,755 loans.6 The median loan amount is $234k; the median LTV is 80%; and the median credit score is 675. The sample consists of 16.4% prime loans, 47.6% subprime loans, and 36% Alt-A, negative amortization, or scratch-and-dent loans. Additionally, 87% of the loans are reported as owner occupied, with the remaining reported as investments or second homes. The proportion of loans with an adjustable rate is 67.4%, and the remaining have a fixed rate. Low/no documentation loans comprise 55.8% of the sample, and full documentation loans comprise 44.2%. With respect to loan performance, 33.1% of the sample loans became seriously delinquent (past due 90 days or more), while 26.1% entered foreclosure before July 2012; 8.2% of the loans entered foreclosure with the borrower not making any payment between the first payment that was missed and the foreclosure date (direct default), and 2.2% of the loans entered early delinquency, meaning that the loan became seriously delinquent within six months of the first payment date.

Sample and variable description

| Panel A: Loan characteristics | |||

|---|---|---|---|

| Mean | Median | SD | |

| Original loan amount | 292,721.6 | 234,000.0 | 203,532.1 |

| Loan-to-value | 76.7 | 80.0 | 13.0 |

| Combined loan-to-value | 79.8 | 80.0 | 14.9 |

| Credit score | 671.5 | 675.0 | 73.6 |

| Original interest rate | 6.6 | 6.7 | 2.2 |

| Panel A: Loan characteristics | |||

|---|---|---|---|

| Mean | Median | SD | |

| Original loan amount | 292,721.6 | 234,000.0 | 203,532.1 |

| Loan-to-value | 76.7 | 80.0 | 13.0 |

| Combined loan-to-value | 79.8 | 80.0 | 14.9 |

| Credit score | 671.5 | 675.0 | 73.6 |

| Original interest rate | 6.6 | 6.7 | 2.2 |

| Panel B: Distribution by characteristics (%) | |||

|---|---|---|---|

| Asset type | Documentation type | ||

| Prime | 16.4 | low/no | 55.8 |

| Subprime | 47.6 | full | 44.2 |

| Alt-A, NegArm, other | 36.0 | other/unreported | - |

| Loan purpose | Reported occupancy status | ||

| purchase | 43.8 | owner occupied | 87.0 |

| refinance | 56.2 | investment/second home | 13.0 |

| Interest rate type | Prepayment penalty | ||

| adjustable | 67.4 | no | 38.4 |

| fixed | 32.6 | yes | 61.6 |

| Panel B: Distribution by characteristics (%) | |||

|---|---|---|---|

| Asset type | Documentation type | ||

| Prime | 16.4 | low/no | 55.8 |

| Subprime | 47.6 | full | 44.2 |

| Alt-A, NegArm, other | 36.0 | other/unreported | - |

| Loan purpose | Reported occupancy status | ||

| purchase | 43.8 | owner occupied | 87.0 |

| refinance | 56.2 | investment/second home | 13.0 |

| Interest rate type | Prepayment penalty | ||

| adjustable | 67.4 | no | 38.4 |

| fixed | 32.6 | yes | 61.6 |

| Panel C: Loan performance (%) | |||

|---|---|---|---|

| delinquent | 33.1 | direct default | 8.2 |

| foreclosure | 26.1 | early delinquency | 2.2 |

| Number of loans | 3,143,755 | ||

| Panel C: Loan performance (%) | |||

|---|---|---|---|

| delinquent | 33.1 | direct default | 8.2 |

| foreclosure | 26.1 | early delinquency | 2.2 |

| Number of loans | 3,143,755 | ||

This table presents descriptive statistics for the main sample. The sample consists of ABSNet-DataQuick-matched securitized first-lien loans used for the purchase of a home with an initial loan amount over $30k and a loan-to-value (LTV) ratio less than or equal to 103%. We drop loans associated with the largest 1% of the transactions in each state, loans reported as being for homes having more than one unit, and loans that belong to MBS deals in which all mortgages are recorded to have an LTV equal to their combined LTV. Panel A presents descriptive statistics for the loan characteristics. Panel B presents the sample distribution by loan characteristic. Panel C describes loan performance.

Sample and variable description

| Panel A: Loan characteristics | |||

|---|---|---|---|

| Mean | Median | SD | |

| Original loan amount | 292,721.6 | 234,000.0 | 203,532.1 |

| Loan-to-value | 76.7 | 80.0 | 13.0 |

| Combined loan-to-value | 79.8 | 80.0 | 14.9 |

| Credit score | 671.5 | 675.0 | 73.6 |

| Original interest rate | 6.6 | 6.7 | 2.2 |

| Panel A: Loan characteristics | |||

|---|---|---|---|

| Mean | Median | SD | |

| Original loan amount | 292,721.6 | 234,000.0 | 203,532.1 |

| Loan-to-value | 76.7 | 80.0 | 13.0 |

| Combined loan-to-value | 79.8 | 80.0 | 14.9 |

| Credit score | 671.5 | 675.0 | 73.6 |

| Original interest rate | 6.6 | 6.7 | 2.2 |

| Panel B: Distribution by characteristics (%) | |||

|---|---|---|---|

| Asset type | Documentation type | ||

| Prime | 16.4 | low/no | 55.8 |

| Subprime | 47.6 | full | 44.2 |

| Alt-A, NegArm, other | 36.0 | other/unreported | - |

| Loan purpose | Reported occupancy status | ||

| purchase | 43.8 | owner occupied | 87.0 |

| refinance | 56.2 | investment/second home | 13.0 |

| Interest rate type | Prepayment penalty | ||

| adjustable | 67.4 | no | 38.4 |

| fixed | 32.6 | yes | 61.6 |

| Panel B: Distribution by characteristics (%) | |||

|---|---|---|---|

| Asset type | Documentation type | ||

| Prime | 16.4 | low/no | 55.8 |

| Subprime | 47.6 | full | 44.2 |

| Alt-A, NegArm, other | 36.0 | other/unreported | - |

| Loan purpose | Reported occupancy status | ||

| purchase | 43.8 | owner occupied | 87.0 |

| refinance | 56.2 | investment/second home | 13.0 |

| Interest rate type | Prepayment penalty | ||

| adjustable | 67.4 | no | 38.4 |

| fixed | 32.6 | yes | 61.6 |

| Panel C: Loan performance (%) | |||

|---|---|---|---|

| delinquent | 33.1 | direct default | 8.2 |

| foreclosure | 26.1 | early delinquency | 2.2 |

| Number of loans | 3,143,755 | ||

| Panel C: Loan performance (%) | |||

|---|---|---|---|

| delinquent | 33.1 | direct default | 8.2 |

| foreclosure | 26.1 | early delinquency | 2.2 |

| Number of loans | 3,143,755 | ||

This table presents descriptive statistics for the main sample. The sample consists of ABSNet-DataQuick-matched securitized first-lien loans used for the purchase of a home with an initial loan amount over $30k and a loan-to-value (LTV) ratio less than or equal to 103%. We drop loans associated with the largest 1% of the transactions in each state, loans reported as being for homes having more than one unit, and loans that belong to MBS deals in which all mortgages are recorded to have an LTV equal to their combined LTV. Panel A presents descriptive statistics for the loan characteristics. Panel B presents the sample distribution by loan characteristic. Panel C describes loan performance.

2. Misrepresentation Indicators and Summary Statistics

2.1 Unreported second lien

A second lien allows a borrower to take additional debt, giving the borrower less incentive to repay the loans and making the initial debt riskier. Therefore, to evaluate the risk of a first-lien loan, it is important to know whether the borrower has a second lien. Accordingly, we construct the dummy variable Unreported second, which takes the value of one if the loan in ABSNet associated with the transaction does not disclose a second lien (i.e., LTV = combined LTV) but both a first and second lien are recorded in county-level records as captured by DataQuick. To be flagged as potentially misreported, we also conservatively require the LTV of the first lien to be greater than or equal to 80%.

2.2 Occupancy misreporting

Borrowers who own and occupy a property are less likely to default than borrowers who do not occupy the property. Consequently, originators charge lower interest rates and require smaller down payments for owner occupants. This gives borrowers and/or originators the incentive to misreport occupancy status.

We are able to estimate occupancy status from county-level transactions using the DataQuick database. We compare the mailing address (where the county sends the tax bill) to the purchased property address. If the mailing address differs from the property address, then we take the property to be a second home or an investment property. Some people might have their taxes sent to their business address or a post office box, so we additionally require that the mailing address not correspond to a commercial address or a PO Box. The variable Occupancy misreporting takes the value of one if the self-reported occupancy status associated with the loan in ABSNet is “owner occupied,” but we estimate otherwise from DataQuick's county-level data. Since owner occupancy status is based on where the purchaser files to have their first tax bill sent, the measure may capture purchasers who later become owner occupants. Piskorski et al. (2015) use credit data that note where a person is having their bills sent. They define a house as nonowner occupied if bills are never sent to the property in the first 12 months after purchase. Their measure is 86% as large as our measure over their sample period, indicating that a limitation of our owner occupancy measure is that it likely captures a small set of late movers who do not occupy the home immediately after purchase but later become owner occupants.

2.3 Appraisal overstatement

If the appraiser gives an inflated appraised value for the property, the borrower can secure a larger loan. If the difference between the appraised value of the property and its fair value is large enough, the borrower can obtain a monetary gain at the expense of the lender by defaulting on the mortgage payments (i.e., misrepresentation for profit). Even if the borrower has no intention to default, the borrower can put less money down (i.e., misrepresentation for housing).

As a proxy for the fair value of a property at the time of origination, we use Lewtan's proprietary AVM.7 In contrast to the two measures above, the AVM originates from models. Both the appraisals and the AVM will have estimation error. Ultimately, it is an empirical question as to whether the appraisals or the AVM is more accurate. If AVMs are more accurate than appraisers, this would suggest that either appraisers made mistakes or appraisals were potentially inflated. Below, we try to separate these two possibilities. Empirically, we show in the Internet Appendix Figure IA. 4 that loan performance considerably deteriorates for appraisals 5% larger than the AVM value. Hence, we use the 5% threshold in some aggregate findings. However, in our more detailed tests that rely upon the measure for other purposes, such as regressions, we use a 20% threshold. We use the higher threshold in subsequent results to account for potential estimation error from the AVM originating from a model, in spite of the findings in the Internet Appendix indicating that this is likely too conservative. We define Misreported as a dummy variable that takes the value of one if one or more of the three misrepresentation indicators is true.

2.4 Summary statistics

The mean values of the misrepresentation indicators defined previously are presented in Table 2. We find that 10.2% of first-lien loans contain a second lien that is not disclosed. This percentage is 13.4% when considered as a fraction of all loans marked with no second lien. The occupancy misreporting indicator appears in 6.7% of the sample. The most common misrepresentation indicator is appraisal overstatements, which appear in 44.9% of loans when using the 5% threshold and in 17.8% of the loans when using the 20% threshold. Aggregating across all indicators, 48.8% of the loans exhibit at least one misreporting indicator (30.1% when using the overly conservative 20% threshold). The correlations between the three misreporting indicators are fairly low (3% on average).

Misreporting variables

| Main sample | Low/no doc | Full doc | Purchase | Refinance | Common sample | |

|---|---|---|---|---|---|---|

| Unreported second | 10.2 | 9.5 | 11.1 | 19.6 | 2.9 | 8.5 |

| Unreported second (from loans reported as having no second lien) | 13.4 | 13.1 | 13.8 | 29.3 | 3.5 | 11.2 |

| Misreported occupancy | 6.7 | 7.2 | 6.0 | 11.7 | 2.6 | 6.0 |

| Misreported occupancy (from loans reported for owner occupancy) | 7.7 | 8.5 | 6.7 | 14.0 | 2.9 | 6.8 |

| Appraisal overstatement | 17.8 | 17.5 | 18.1 | 13.2 | 20.5 | 17.8 |

| Appraisal overstatement (using a 5% threshold) | 44.9 | 44.3 | 45.7 | 36.5 | 49.9 | 43.8 |

| Misreported | 30.1 | 29.6 | 30.6 | 35.9 | 25.6 | 29.3 |

| Misreported (using a 5% threshold) | 48.8 | 48.0 | 49.8 | 47.0 | 50.2 | 51.9 |

| Main sample | Low/no doc | Full doc | Purchase | Refinance | Common sample | |

|---|---|---|---|---|---|---|

| Unreported second | 10.2 | 9.5 | 11.1 | 19.6 | 2.9 | 8.5 |

| Unreported second (from loans reported as having no second lien) | 13.4 | 13.1 | 13.8 | 29.3 | 3.5 | 11.2 |

| Misreported occupancy | 6.7 | 7.2 | 6.0 | 11.7 | 2.6 | 6.0 |

| Misreported occupancy (from loans reported for owner occupancy) | 7.7 | 8.5 | 6.7 | 14.0 | 2.9 | 6.8 |

| Appraisal overstatement | 17.8 | 17.5 | 18.1 | 13.2 | 20.5 | 17.8 |

| Appraisal overstatement (using a 5% threshold) | 44.9 | 44.3 | 45.7 | 36.5 | 49.9 | 43.8 |

| Misreported | 30.1 | 29.6 | 30.6 | 35.9 | 25.6 | 29.3 |

| Misreported (using a 5% threshold) | 48.8 | 48.0 | 49.8 | 47.0 | 50.2 | 51.9 |

This table presents means for the misreporting variables (in percent). We construct three mortgage misreporting indicators to capture unreported second liens, occupancy status misreporting, and appraisal overstatements. Unreported second is a dummy variable that takes the value of one if the loan in ABSNet associated with the transaction does not disclose the existence of a second lien (i.e., LTV = combined LTV) but both a first and a second lien are recorded in county-level records as reflected by DataQuick. Occupancy misreporting is a dummy variable that takes the value of one if the self-reported occupancy status associated with the loan in ABSNet (using data from MBS prospectus documents) is marked as “owner occupied,” but we estimate otherwise from DataQuick's county-level data. Appraisal overstatement is a dummy variable that takes the value of one if the appraised value recorded before origination exceeded ABSNet's AVM value by more than 20%. Misreported is a dummy variable that takes the value of one if one or more of the four misreporting indicators is true.

Misreporting variables

| Main sample | Low/no doc | Full doc | Purchase | Refinance | Common sample | |

|---|---|---|---|---|---|---|

| Unreported second | 10.2 | 9.5 | 11.1 | 19.6 | 2.9 | 8.5 |

| Unreported second (from loans reported as having no second lien) | 13.4 | 13.1 | 13.8 | 29.3 | 3.5 | 11.2 |

| Misreported occupancy | 6.7 | 7.2 | 6.0 | 11.7 | 2.6 | 6.0 |

| Misreported occupancy (from loans reported for owner occupancy) | 7.7 | 8.5 | 6.7 | 14.0 | 2.9 | 6.8 |

| Appraisal overstatement | 17.8 | 17.5 | 18.1 | 13.2 | 20.5 | 17.8 |

| Appraisal overstatement (using a 5% threshold) | 44.9 | 44.3 | 45.7 | 36.5 | 49.9 | 43.8 |

| Misreported | 30.1 | 29.6 | 30.6 | 35.9 | 25.6 | 29.3 |

| Misreported (using a 5% threshold) | 48.8 | 48.0 | 49.8 | 47.0 | 50.2 | 51.9 |

| Main sample | Low/no doc | Full doc | Purchase | Refinance | Common sample | |

|---|---|---|---|---|---|---|

| Unreported second | 10.2 | 9.5 | 11.1 | 19.6 | 2.9 | 8.5 |

| Unreported second (from loans reported as having no second lien) | 13.4 | 13.1 | 13.8 | 29.3 | 3.5 | 11.2 |

| Misreported occupancy | 6.7 | 7.2 | 6.0 | 11.7 | 2.6 | 6.0 |

| Misreported occupancy (from loans reported for owner occupancy) | 7.7 | 8.5 | 6.7 | 14.0 | 2.9 | 6.8 |

| Appraisal overstatement | 17.8 | 17.5 | 18.1 | 13.2 | 20.5 | 17.8 |

| Appraisal overstatement (using a 5% threshold) | 44.9 | 44.3 | 45.7 | 36.5 | 49.9 | 43.8 |

| Misreported | 30.1 | 29.6 | 30.6 | 35.9 | 25.6 | 29.3 |

| Misreported (using a 5% threshold) | 48.8 | 48.0 | 49.8 | 47.0 | 50.2 | 51.9 |

This table presents means for the misreporting variables (in percent). We construct three mortgage misreporting indicators to capture unreported second liens, occupancy status misreporting, and appraisal overstatements. Unreported second is a dummy variable that takes the value of one if the loan in ABSNet associated with the transaction does not disclose the existence of a second lien (i.e., LTV = combined LTV) but both a first and a second lien are recorded in county-level records as reflected by DataQuick. Occupancy misreporting is a dummy variable that takes the value of one if the self-reported occupancy status associated with the loan in ABSNet (using data from MBS prospectus documents) is marked as “owner occupied,” but we estimate otherwise from DataQuick's county-level data. Appraisal overstatement is a dummy variable that takes the value of one if the appraised value recorded before origination exceeded ABSNet's AVM value by more than 20%. Misreported is a dummy variable that takes the value of one if one or more of the four misreporting indicators is true.

Appraisals can be understated as well. Nevertheless, as shown in the Internet Appendix, the distribution of appraisal overstatements is neither symmetric nor centered at 0%. Inconsistent with random appraisal errors, we find that 44.9% of the loans show appraisals that are 5% or above the AVM, but only 23.3% of the loans show the AVM being 5% or above the appraised value.8

Additionally, unreported second liens and occupancy misreporting are considerably higher in purchases than in refinances. The opposite is true for appraisal overstatements. This is interesting since appraisals are the sole determinant of the transaction price with refinances. Lenders would also presumably be aware if the house was owner occupied or had a second lien with a refinance. Interestingly, misreporting does not seem to be a simple function of available information at origination. Both unreported second liens and appraisal overstatements are slightly higher in full documentation loans than in low/no documentation loans (1.6% and 0.6% higher, respectively).

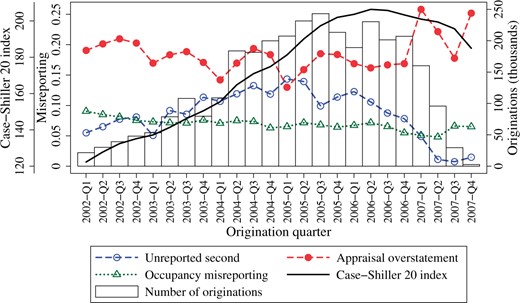

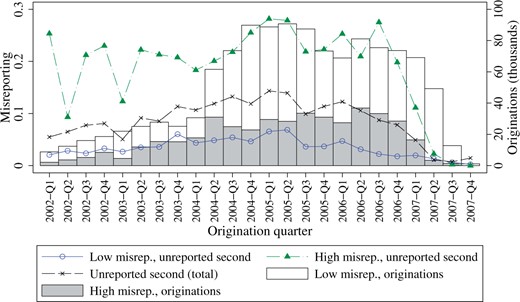

Figure 1 shows the evolution of the different misrepresentation indicators by quarter for the period from 2002 to 2007. The prevalence of unreported second liens increases rapidly and peaks about a year before the top of the housing market in the first quarter of 2005. Owner occupancy misreporting appears to gradually decrease from an average of 8.3% in 2002 to an average of 5.1% at the beginning of 2007. Appraisal overstatement varies but remains at high levels throughout the period.

Misreporting indicators by quarter

This figure shows the evolution of the different misreporting indicators by quarter. The indicators Unreported second, Occupancy misreporting, and Appraisal overstatement are defined in Table 2. The bars represent the number of first-lien loan originations in each quarter, and the black line shows the evolution of housing prices as captured by the Case-Shiller 20 Index. The main sample consists of ABSNet-DataQuick-matched securitized first-lien loans used for the purchase or refinance of a home with an initial loan amount over $30k and a loan-to-value (LTV) ratio less than or equal to 103%. We drop loans associated with the largest 1% of the transactions in each state, loans reported as having more than one unit, and loans that belong to MBS deals in which all mortgages are recorded to have an LTV equal to their combined LTV.

In the second and third quarters of 2007, the prevalence of unreported second liens plummets. Since reported second-lien origination stays at a similar high level, the drop is not due to a decline in second-lien origination.

3. Does Misreporting Affect Loan Performance?

In the previous section we present evidence consistent with an extremely large amount of potential misrepresentation. However, our measures need external validation. If the indicators are capturing mortgage misreporting, then the misreported loans should underperform loans that are not affected by misreporting or misrepresentation. In most of our tests we focus on serious delinquencies, followed by direct defaults, as our measure of loan performance.

3.1 Summary analysis

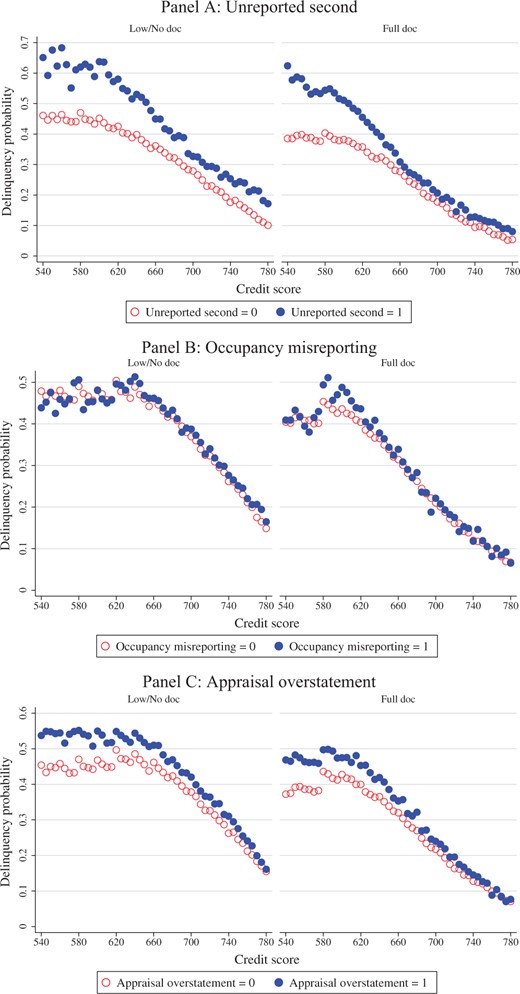

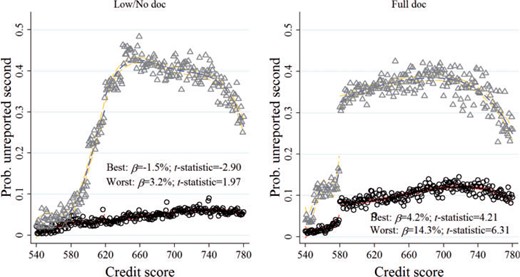

Figure 2 depicts loan performance over the credit score spectrum, separated by low/no documentation loans and full documentation loans. Panel A shows that the delinquency effect is strong for second-lien misreporting. Misreporting is strongly related to delinquencies across all ranges of the credit score distribution, but particularly for low credit scores. The relationship is considerably weaker for occupancy misreporting (panel B). The effect is strong for appraisal overstatements (panel C).

Probability of delinquency by credit score bin

This figure compares the probability of delinquency by credit score bin of loans that exhibit misreporting (solid circles) and loans that do not exhibit misreporting (hollow circles). Each credit score bin has a size of five units. We construct three mortgage misreporting indicators to capture unreported second liens, occupancy status misreporting, and appraisal overstatements (the indicators are defined in Table 2). The comparisons based on unreported second liens, occupancy misreporting, and appraisal overstatements are shown in panels A, B, and C, respectively.

3.2 Regression analysis

We now turn to a more formal framework. We estimate logit regressions in which the dependent variable is the delinquency dummy and the independent variables of interest are the different misreporting indicators. To ensure that our misrepresentation variable is not simply capturing a correlation with some other aspect of loan riskiness, we control for the typical determinants of loan performance found in previous literature (Mayer, Pence, and Sherlund 2009). In addition, we include controls for complex mortgages, the original interest rate (fixed- and adjustable-rate mortgages), reported second liens, and reported occupancy status.9 To allow coefficients to be interpreted more easily, all continuous variables are standardized by subtracting their mean and dividing by their standard deviation. CBSA-quarter fixed effects are included in all specifications to ensure that our variables are not capturing some correlated aspect of regional home price movements. We also cluster standard errors by CBSA-quarter. Results in Table 3, panel A, show the odds ratios and z-statistics (in parentheses) of the regressions when including Unreported second in the set of explanatory variables. After controlling for the strict set of controls and fixed effects, we find that a first lien that has an unreported second lien is 97% more likely to become seriously delinquent than loans that were not misreported. The strong effect on loan performance of our indicator of second-lien misreporting is not driven by loans originated in California or Florida, since the odds ratio remains exactly the same when excluding these two states from the main sample. Panels B and C show that the effect of occupancy misreporting and appraisal overstatements on loan performance is lower than the effect of unreported second liens, though it is still important. Loans that misreport their occupancy status are 8% more likely to become delinquent than truthfully reported loans. The effect of appraisal overstatements is also material. Loans that have appraisals 20% or higher than the AVM at the time of origination are 34% more likely to become delinquent. Results are not driven by loans originated in California or Florida. Panel D presents results when using our aggregate indicator of misreporting. A misreported loan is associated with a 51% higher likelihood of becoming delinquent. The effect of all the misreporting indicators is also economically and statistically significant when analyzing purchases and refinances separately. Finally, using a common sample in which all loans are required to have all three misreporting indicators, the regressions confirm that the misreporting indicator with the most influence on performance is Unreported second, followed by Appraisal overstatement and then Occupancy misreporting. Interestingly, the reported variables are important in predicting delinquencies, demonstrating that not all information in the structured finance space was useless. Tinkering with an indicator that predicts default would be valuable if one were to engage in misreporting.

Effect of misreporting on delinquency

| Panel A: Unreported second | |||||

|---|---|---|---|---|---|

| Main sample | Main sample ex CA, FL | Common sample | Purchases | Refinances | |

| Unreported second | 1.97*** | 1.97*** | 2.13*** | 2.03*** | 1.81*** |

| (50.26) | (46.50) | (54.38) | (39.90) | (40.99) | |

| Reported second | 2.14*** | 2.10*** | 2.06*** | 2.63*** | 1.65*** |

| (90.00) | (61.29) | (88.55) | (72.93) | (59.84) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 3,140,472 | 1,687,283 | 2,306,331 | 1,371,552 | 1,764,505 |

| Pseudo | 0.26 | 0.21 | 0.26 | 0.28 | 0.25 |

| Panel A: Unreported second | |||||

|---|---|---|---|---|---|

| Main sample | Main sample ex CA, FL | Common sample | Purchases | Refinances | |

| Unreported second | 1.97*** | 1.97*** | 2.13*** | 2.03*** | 1.81*** |

| (50.26) | (46.50) | (54.38) | (39.90) | (40.99) | |

| Reported second | 2.14*** | 2.10*** | 2.06*** | 2.63*** | 1.65*** |

| (90.00) | (61.29) | (88.55) | (72.93) | (59.84) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 3,140,472 | 1,687,283 | 2,306,331 | 1,371,552 | 1,764,505 |

| Pseudo | 0.26 | 0.21 | 0.26 | 0.28 | 0.25 |

| Panel B: Occupancy misreporting | |||||

|---|---|---|---|---|---|

| Occupancy misreporting | 1.08*** | 1.14*** | 1.08*** | 1.06*** | 1.05*** |

| (7.18) | (9.99) | (6.67) | (5.00) | (3.38) | |

| Reported nonowner occupied | 1.15*** | 1.30*** | 1.16*** | 0.93*** | 1.46*** |

| (10.43) | (19.97) | (11.35) | (-3.99) | (30.60) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 2,807,954 | 1,391,821 | 2,306,331 | 1,252,643 | 1,551,027 |

| Pseudo | 0.25 | 0.20 | 0.25 | 0.27 | 0.25 |

| Panel B: Occupancy misreporting | |||||

|---|---|---|---|---|---|

| Occupancy misreporting | 1.08*** | 1.14*** | 1.08*** | 1.06*** | 1.05*** |

| (7.18) | (9.99) | (6.67) | (5.00) | (3.38) | |

| Reported nonowner occupied | 1.15*** | 1.30*** | 1.16*** | 0.93*** | 1.46*** |

| (10.43) | (19.97) | (11.35) | (-3.99) | (30.60) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 2,807,954 | 1,391,821 | 2,306,331 | 1,252,643 | 1,551,027 |

| Pseudo | 0.25 | 0.20 | 0.25 | 0.27 | 0.25 |

| Panel C: Appraisal overstatement | |||||

|---|---|---|---|---|---|

| Appraisal overstatement | 1.34*** | 1.36*** | 1.34*** | 1.50*** | 1.23*** |

| (46.57) | (43.33) | (43.30) | (31.51) | (31.66) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 2,576,423 | 1,334,103 | 2,306,331 | 949,997 | 1,622,278 |

| Pseudo | 0.25 | 0.20 | 0.25 | 0.27 | 0.25 |

| Panel C: Appraisal overstatement | |||||

|---|---|---|---|---|---|

| Appraisal overstatement | 1.34*** | 1.36*** | 1.34*** | 1.50*** | 1.23*** |

| (46.57) | (43.33) | (43.30) | (31.51) | (31.66) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 2,576,423 | 1,334,103 | 2,306,331 | 949,997 | 1,622,278 |

| Pseudo | 0.25 | 0.20 | 0.25 | 0.27 | 0.25 |

| Panel D: Misreported | |||||

|---|---|---|---|---|---|

| Misreported | 1.51*** | 1.53*** | 1.49*** | 1.69*** | 1.30*** |

| (64.50) | (62.09) | (59.57) | (46.33) | (43.59) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 3,141,156 | 1,687,666 | 2,306,331 | 1,371,613 | 1,765,126 |

| Pseudo | 0.25 | 0.21 | 0.26 | 0.28 | 0.25 |

| Panel D: Misreported | |||||

|---|---|---|---|---|---|

| Misreported | 1.51*** | 1.53*** | 1.49*** | 1.69*** | 1.30*** |

| (64.50) | (62.09) | (59.57) | (46.33) | (43.59) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 3,141,156 | 1,687,666 | 2,306,331 | 1,371,613 | 1,765,126 |

| Pseudo | 0.25 | 0.21 | 0.26 | 0.28 | 0.25 |

This table presents the odds ratios of logit regressions in which the dependent variable is Delinquent, a dummy variable that takes the value of one if the loan was more than 90 days late. Panels A, B, C, and D show the results for unreported second liens, occupancy status misreporting, appraisal overstatements, and aggregated misreporting, respectively. The variables Unreported second, Occupancy misreporting, Appraisal overstatement, and Misreported are defined in Table 2. The set of controls includes Reported second, a dummy variable that takes the value of one if the loan is reported as having a second lien (i.e., LTV≠ combined LTV), and Reported nonowner occupant, a dummy variable that takes the value of one if the loan is reported to be for an investment property or a second home. Additional controls include controls for low/no doc loans, loans used for refinancing, the borrower's credit score, loan amount, LTV, interest rate at origination, presence of a prepayment penalty, adjustable-rate loans, and complex loans. All continuous variables are standardized by subtracting their means and dividing by their standard deviations. All regressions include core-based statistical area (CBSA) times quarter of origination fixed effects (CBSA × Quarter FE). Standard errors are clustered by CBSA × quarter of origination. The coefficients for all the additional controls are reported in the Internet Appendix. z-statistics are presented in parentheses. , , .

Effect of misreporting on delinquency

| Panel A: Unreported second | |||||

|---|---|---|---|---|---|

| Main sample | Main sample ex CA, FL | Common sample | Purchases | Refinances | |

| Unreported second | 1.97*** | 1.97*** | 2.13*** | 2.03*** | 1.81*** |

| (50.26) | (46.50) | (54.38) | (39.90) | (40.99) | |

| Reported second | 2.14*** | 2.10*** | 2.06*** | 2.63*** | 1.65*** |

| (90.00) | (61.29) | (88.55) | (72.93) | (59.84) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 3,140,472 | 1,687,283 | 2,306,331 | 1,371,552 | 1,764,505 |

| Pseudo | 0.26 | 0.21 | 0.26 | 0.28 | 0.25 |

| Panel A: Unreported second | |||||

|---|---|---|---|---|---|

| Main sample | Main sample ex CA, FL | Common sample | Purchases | Refinances | |

| Unreported second | 1.97*** | 1.97*** | 2.13*** | 2.03*** | 1.81*** |

| (50.26) | (46.50) | (54.38) | (39.90) | (40.99) | |

| Reported second | 2.14*** | 2.10*** | 2.06*** | 2.63*** | 1.65*** |

| (90.00) | (61.29) | (88.55) | (72.93) | (59.84) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 3,140,472 | 1,687,283 | 2,306,331 | 1,371,552 | 1,764,505 |

| Pseudo | 0.26 | 0.21 | 0.26 | 0.28 | 0.25 |

| Panel B: Occupancy misreporting | |||||

|---|---|---|---|---|---|

| Occupancy misreporting | 1.08*** | 1.14*** | 1.08*** | 1.06*** | 1.05*** |

| (7.18) | (9.99) | (6.67) | (5.00) | (3.38) | |

| Reported nonowner occupied | 1.15*** | 1.30*** | 1.16*** | 0.93*** | 1.46*** |

| (10.43) | (19.97) | (11.35) | (-3.99) | (30.60) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 2,807,954 | 1,391,821 | 2,306,331 | 1,252,643 | 1,551,027 |

| Pseudo | 0.25 | 0.20 | 0.25 | 0.27 | 0.25 |

| Panel B: Occupancy misreporting | |||||

|---|---|---|---|---|---|

| Occupancy misreporting | 1.08*** | 1.14*** | 1.08*** | 1.06*** | 1.05*** |

| (7.18) | (9.99) | (6.67) | (5.00) | (3.38) | |

| Reported nonowner occupied | 1.15*** | 1.30*** | 1.16*** | 0.93*** | 1.46*** |

| (10.43) | (19.97) | (11.35) | (-3.99) | (30.60) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 2,807,954 | 1,391,821 | 2,306,331 | 1,252,643 | 1,551,027 |

| Pseudo | 0.25 | 0.20 | 0.25 | 0.27 | 0.25 |

| Panel C: Appraisal overstatement | |||||

|---|---|---|---|---|---|

| Appraisal overstatement | 1.34*** | 1.36*** | 1.34*** | 1.50*** | 1.23*** |

| (46.57) | (43.33) | (43.30) | (31.51) | (31.66) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 2,576,423 | 1,334,103 | 2,306,331 | 949,997 | 1,622,278 |

| Pseudo | 0.25 | 0.20 | 0.25 | 0.27 | 0.25 |

| Panel C: Appraisal overstatement | |||||

|---|---|---|---|---|---|

| Appraisal overstatement | 1.34*** | 1.36*** | 1.34*** | 1.50*** | 1.23*** |

| (46.57) | (43.33) | (43.30) | (31.51) | (31.66) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 2,576,423 | 1,334,103 | 2,306,331 | 949,997 | 1,622,278 |

| Pseudo | 0.25 | 0.20 | 0.25 | 0.27 | 0.25 |

| Panel D: Misreported | |||||

|---|---|---|---|---|---|

| Misreported | 1.51*** | 1.53*** | 1.49*** | 1.69*** | 1.30*** |

| (64.50) | (62.09) | (59.57) | (46.33) | (43.59) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 3,141,156 | 1,687,666 | 2,306,331 | 1,371,613 | 1,765,126 |

| Pseudo | 0.25 | 0.21 | 0.26 | 0.28 | 0.25 |

| Panel D: Misreported | |||||

|---|---|---|---|---|---|

| Misreported | 1.51*** | 1.53*** | 1.49*** | 1.69*** | 1.30*** |

| (64.50) | (62.09) | (59.57) | (46.33) | (43.59) | |

| Controls | yes | yes | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes | yes | yes |

| Observations | 3,141,156 | 1,687,666 | 2,306,331 | 1,371,613 | 1,765,126 |

| Pseudo | 0.25 | 0.21 | 0.26 | 0.28 | 0.25 |

This table presents the odds ratios of logit regressions in which the dependent variable is Delinquent, a dummy variable that takes the value of one if the loan was more than 90 days late. Panels A, B, C, and D show the results for unreported second liens, occupancy status misreporting, appraisal overstatements, and aggregated misreporting, respectively. The variables Unreported second, Occupancy misreporting, Appraisal overstatement, and Misreported are defined in Table 2. The set of controls includes Reported second, a dummy variable that takes the value of one if the loan is reported as having a second lien (i.e., LTV≠ combined LTV), and Reported nonowner occupant, a dummy variable that takes the value of one if the loan is reported to be for an investment property or a second home. Additional controls include controls for low/no doc loans, loans used for refinancing, the borrower's credit score, loan amount, LTV, interest rate at origination, presence of a prepayment penalty, adjustable-rate loans, and complex loans. All continuous variables are standardized by subtracting their means and dividing by their standard deviations. All regressions include core-based statistical area (CBSA) times quarter of origination fixed effects (CBSA × Quarter FE). Standard errors are clustered by CBSA × quarter of origination. The coefficients for all the additional controls are reported in the Internet Appendix. z-statistics are presented in parentheses. , , .

We find similar results when using foreclosures and early delinquencies (as shown in the Internet Appendix) as performance variables.

4. What Is the Role of Borrowers, Appraisers, Lenders, and Underwriters in Misreporting?

In this section we use a variety of empirical methods to examine what we can learn about who seemed to be aware of the misreporting.

4.1 Was misreporting adequately priced by lenders?

If lenders take loan features into account when they set interest rates, then this will suggest that they recognize when loans have a higher level of risk. To test this conjecture, we regress loan interest rate at origination against the misreporting indicators and our strict set of loan level controls and fixed effects. Table 4 reports the coefficient estimates for the variables of interest (t-statistics in parentheses). Panel A shows that second-lien misreporting, which is most prominent and impacts performance the most, is also associated with the largest increase in interest rates (14 bps). This result indicates that lenders knew about undisclosed second-lien loans. Indeed, the interest rate charged is 4 bps larger than that on loans with reported second-lien loans (the difference is statistically significant, with an F-statistic of 25.37). Loans with occupancy misreporting (panel B) are 5 bps higher on average. The interest rate is significantly less than that on loans reported as investments or second homes. Loans that exhibit appraisal overstatements appear to have a slightly higher interest rate at origination on average (7 bps). In summary, we find that lenders detect and internalize unreported second liens, and, to a lesser extent, appraisal overstatements. With respect to occupancy misreporting, it seems to be instigated by buyers, or originating lenders do not require extra compensation for loans associated with owner-occupied purchases that may not be the borrower's primary residence.

Effect of misreporting on the interest rate at origination

| Panel A: Unreported second | |||

|---|---|---|---|

| Main sample | Main sample ex CA, FL | Common sample | |

| Unreported second | 0.14*** | 0.10*** | 0.14*** |

| (19.35) | (11.48) | (15.33) | |

| Reported second | 0.10*** | 0.06*** | 0.09*** |

| (11.31) | (7.72) | (9.81) | |

| Controls | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes |

| Observations | 3,140,472 | 1,687,283 | 2,306,331 |

| Adj. | 0.62 | 0.60 | 0.62 |

| Panel A: Unreported second | |||

|---|---|---|---|

| Main sample | Main sample ex CA, FL | Common sample | |

| Unreported second | 0.14*** | 0.10*** | 0.14*** |

| (19.35) | (11.48) | (15.33) | |

| Reported second | 0.10*** | 0.06*** | 0.09*** |

| (11.31) | (7.72) | (9.81) | |

| Controls | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes |

| Observations | 3,140,472 | 1,687,283 | 2,306,331 |

| Adj. | 0.62 | 0.60 | 0.62 |

| Panel B: Occupancy misreporting | |||

|---|---|---|---|

| Occupancy misreporting | 0.05*** | 0.07*** | 0.04*** |

| (9.73) | (11.19) | (8.51) | |

| Reported nonowner occupied | 0.32*** | 0.42*** | 0.32*** |

| (45.54) | (54.41) | (43.51) | |

| Controls | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes |

| Observations | 2,807,954 | 1,391,821 | 2,306,331 |

| Adj. | 0.63 | 0.60 | 0.62 |

| Panel B: Occupancy misreporting | |||

|---|---|---|---|

| Occupancy misreporting | 0.05*** | 0.07*** | 0.04*** |

| (9.73) | (11.19) | (8.51) | |

| Reported nonowner occupied | 0.32*** | 0.42*** | 0.32*** |

| (45.54) | (54.41) | (43.51) | |

| Controls | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes |

| Observations | 2,807,954 | 1,391,821 | 2,306,331 |

| Adj. | 0.63 | 0.60 | 0.62 |

| Panel C: Appraisal overstatement | |||

|---|---|---|---|

| Appraisal overstatement | 0.07*** | 0.09*** | 0.07*** |

| (25.37) | (23.82) | (23.52) | |

| Controls | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes |

| Observations | 2,576,423 | 1,334,103 | 2,306,331 |

| Adj. | 0.62 | 0.60 | 0.62 |

| Panel C: Appraisal overstatement | |||

|---|---|---|---|

| Appraisal overstatement | 0.07*** | 0.09*** | 0.07*** |

| (25.37) | (23.82) | (23.52) | |

| Controls | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes |

| Observations | 2,576,423 | 1,334,103 | 2,306,331 |

| Adj. | 0.62 | 0.60 | 0.62 |

This table presents OLS regressions in which the dependent variable is the interest rate at origination. Panels A, B, and C show the results for unreported second liens, occupancy status misreporting, and appraisal overstatements, respectively. The variables Unreported second, Occupancy misreporting, and Appraisal overstatement are defined in Table 2. The set of controls includes Reported second, a dummy variable that takes the value of one if the loan is reported as having a second lien (i.e., LTV≠ combined LTV), and Reported nonowner occupant, a dummy variable that takes the value of one if the loan is reported to be for investment property or a second home. Additional controls include controls for low/no doc loans, loans used for refinancing, the borrower's credit score, loan amount, LTV, interest rate at origination, presence of a prepayment penalty, adjustable-rate loans, and complex loans. LTV is separated into two components: values of 80 or lower (LTV Low) and values over 80 (LTV High). All continuous variables are standardized by subtracting their means and dividing by their standard deviations. All regressions include core-based statistical area (CBSA) times quarter of origination fixed effects (CBSA × Quarter FE). Standard errors are clustered by CBSA × quarter of origination. The coefficients for all the additional controls are reported in the Internet Appendix. t-statistics are presented in parentheses. , , .

Effect of misreporting on the interest rate at origination

| Panel A: Unreported second | |||

|---|---|---|---|

| Main sample | Main sample ex CA, FL | Common sample | |

| Unreported second | 0.14*** | 0.10*** | 0.14*** |

| (19.35) | (11.48) | (15.33) | |

| Reported second | 0.10*** | 0.06*** | 0.09*** |

| (11.31) | (7.72) | (9.81) | |

| Controls | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes |

| Observations | 3,140,472 | 1,687,283 | 2,306,331 |

| Adj. | 0.62 | 0.60 | 0.62 |

| Panel A: Unreported second | |||

|---|---|---|---|

| Main sample | Main sample ex CA, FL | Common sample | |

| Unreported second | 0.14*** | 0.10*** | 0.14*** |

| (19.35) | (11.48) | (15.33) | |

| Reported second | 0.10*** | 0.06*** | 0.09*** |

| (11.31) | (7.72) | (9.81) | |

| Controls | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes |

| Observations | 3,140,472 | 1,687,283 | 2,306,331 |

| Adj. | 0.62 | 0.60 | 0.62 |

| Panel B: Occupancy misreporting | |||

|---|---|---|---|

| Occupancy misreporting | 0.05*** | 0.07*** | 0.04*** |

| (9.73) | (11.19) | (8.51) | |

| Reported nonowner occupied | 0.32*** | 0.42*** | 0.32*** |

| (45.54) | (54.41) | (43.51) | |

| Controls | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes |

| Observations | 2,807,954 | 1,391,821 | 2,306,331 |

| Adj. | 0.63 | 0.60 | 0.62 |

| Panel B: Occupancy misreporting | |||

|---|---|---|---|

| Occupancy misreporting | 0.05*** | 0.07*** | 0.04*** |

| (9.73) | (11.19) | (8.51) | |

| Reported nonowner occupied | 0.32*** | 0.42*** | 0.32*** |

| (45.54) | (54.41) | (43.51) | |

| Controls | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes |

| Observations | 2,807,954 | 1,391,821 | 2,306,331 |

| Adj. | 0.63 | 0.60 | 0.62 |

| Panel C: Appraisal overstatement | |||

|---|---|---|---|

| Appraisal overstatement | 0.07*** | 0.09*** | 0.07*** |

| (25.37) | (23.82) | (23.52) | |

| Controls | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes |

| Observations | 2,576,423 | 1,334,103 | 2,306,331 |

| Adj. | 0.62 | 0.60 | 0.62 |

| Panel C: Appraisal overstatement | |||

|---|---|---|---|

| Appraisal overstatement | 0.07*** | 0.09*** | 0.07*** |

| (25.37) | (23.82) | (23.52) | |

| Controls | yes | yes | yes |

| CBSA × Quarter FE | yes | yes | yes |

| Observations | 2,576,423 | 1,334,103 | 2,306,331 |

| Adj. | 0.62 | 0.60 | 0.62 |

This table presents OLS regressions in which the dependent variable is the interest rate at origination. Panels A, B, and C show the results for unreported second liens, occupancy status misreporting, and appraisal overstatements, respectively. The variables Unreported second, Occupancy misreporting, and Appraisal overstatement are defined in Table 2. The set of controls includes Reported second, a dummy variable that takes the value of one if the loan is reported as having a second lien (i.e., LTV≠ combined LTV), and Reported nonowner occupant, a dummy variable that takes the value of one if the loan is reported to be for investment property or a second home. Additional controls include controls for low/no doc loans, loans used for refinancing, the borrower's credit score, loan amount, LTV, interest rate at origination, presence of a prepayment penalty, adjustable-rate loans, and complex loans. LTV is separated into two components: values of 80 or lower (LTV Low) and values over 80 (LTV High). All continuous variables are standardized by subtracting their means and dividing by their standard deviations. All regressions include core-based statistical area (CBSA) times quarter of origination fixed effects (CBSA × Quarter FE). Standard errors are clustered by CBSA × quarter of origination. The coefficients for all the additional controls are reported in the Internet Appendix. t-statistics are presented in parentheses. , , .

4.2 Did securitization provide incentives to misreport?

If misrepresentation increases around a credit score used for securitization, then the originator may be intentionally or unintentionally facilitating borrowing with improper disclosure to obtain loans with the objective of securitizing. If there is no jump in the amount of misrepresentation around the credit score threshold, then the misrepresentation is unlikely to be a function of the originator screening process.

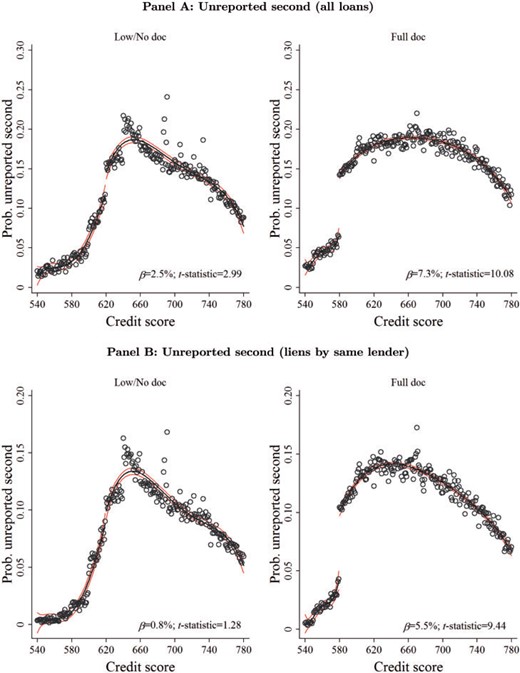

As background, we find results similar to those of Keys et al. (2010): low/no documentation loans whose associated credit score is slightly over 620 are significantly more likely to be securitized.10Keys et al. (2010) focus on delinquencies around the thresholds, whereas we focus on the amount of potential misrepresentation around the thresholds.

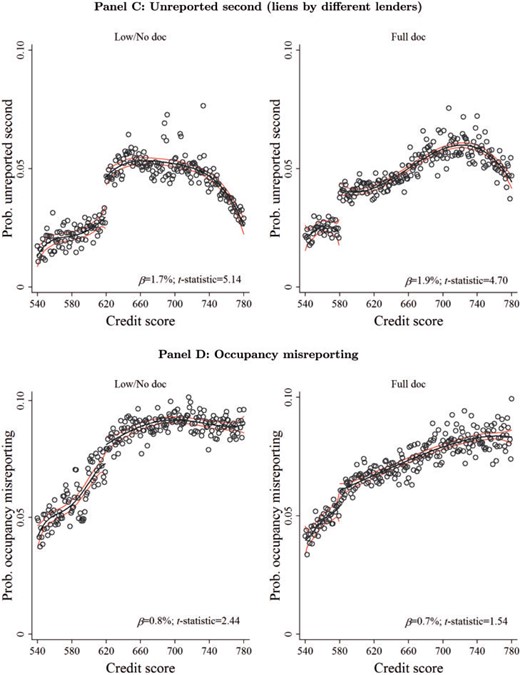

Panel A of Figure 3 displays the results for unreported second liens. Unreported second liens increase significantly in loans with credit scores of 620 compared to loans with a credit score of 619, for both low/no doc and full doc loans. The percentage of unreported second liens increases by 2.5% for low/no doc loans and 7.3% for full doc loans. This result suggests that this type of misreporting derives from the originator's incentives to securitize. We find a small significant increase of 0.8% in the amount of occupancy misreporting only in low/no documentation loans (panel D). We do not find a significant increase in the amount of misreporting for appraisal overstatement (see the Internet Appendix). This evidence suggests that these forms of misreporting are not directly related to the originator's motive to securitize.

Probability of second-lien and occupancy status misreporting around credit score thresholds

This figure shows the probability of second-lien and occupancy status misreporting by credit score. The hollow circles represent the average probability of misreporting for each credit score. The dark black line fits a fourth-order polynomial approximation at both sides of the credit score threshold (620 for low/no documentation loans and 580 for full documentation loans). The light lines delimit the 95% confidence level interval for the approximation. Panel A considers second-lien misreporting when the first-second lien pair was originated either by the same lender or a different lender (all loans). Panels B and C present results for the decomposition of second-lien misreporting. Specifically, panel B shows the probability of second-lien misreporting when the first-second lien pair was originated by the same lender, and panel C shows the probability of second-lien misreporting when the first-second lien pair was originated by different lenders. Panel D shows results for occupancy misreporting. The exact magnitude of the jumps at the discontinuities () along with their t-statistics are also shown in the graphs. The corresponding regression results are shown in the Internet Appendix.

4.3 Was second-lien misreporting facilitated unintentionally or intentionally?

The jumps in the probability of second-lien misreporting at the credit score threshold in low/no doc and full doc loans suggest that originators facilitated misreporting either unintentionally (lax screening process) or intentionally (misrepresentation). To distinguish between these two possible explanations, we further decompose our unreported second-lien indicator into two components: (1) unreported second liens in which the second lien was originated by the same lender that originated the first lien, and (2) unreported second liens in which the second lien was originated by a different lender than the one that originated the first lien. Of the 10.2% of loans associated with second-lien misreporting in our sample, 67.6% (6.9% /10.2%) consist of cases in which the same lender originated the first-second lien pair. In the remaining cases the first and second liens had different originators. The fact that more than two-thirds of the second-lien misreporting occurs among loans originated by the same lender is surprising. Unless the bank had extremely poor record keeping, the issuer should have known about the second lien. The second-lien misreporting is thus likely due to intentional misreporting, either by the originators or by MBS underwriters who realize the loan has a second lien but do not report this information to investors.

We repeat the RDD analysis discussed above for the two types of second-lien misreporting. Panels B and C of Figure 3 display the discontinuity results for the same originator and different originators. Panel B shows that when the same originator is on both the first and the second lien, there is a misreporting jump of 5.5% (significant at the 1% level) at the credit score threshold of 580. For low/no doc loans, the amount of misreporting increases rapidly beyond the credit score threshold of 620, reaching the same levels present in full doc loans above 580. Nevertheless, because of the scattered loan pools between the 600 and 620 marks, there is no statistically detectable jump in the case of low/no doc loans. Likewise, panel C shows that when different originators issue the first and second liens, there continues to be a significant jump in second-lien misreporting (1.7% for low/no doc loans and 1.9% for full doc loans). These results confirm that second-lien misreporting is due at least in part to the incentives of the lender to securitize the loan.

It remains unclear whether the misreporting is due to the loan originator or the bank underwriter. It could be the case that the originators intended to securitize and reported the second-lien information properly to the bank underwriters, who later did not report it. To shed light on whether the misreporting was driven by loan originators or MBS underwriters, we regress our misreporting indicators on loan originator and underwriter fixed effects. If loan originators contributed more to a certain type of misreporting, then the loan originator fixed effects should be more important in explaining the indicator for that type of misreporting, while if underwriting practices contributed more, then underwriter fixed effects should explain more of the misreporting variation.

In Table 5 we also include CBSA-quarter fixed effects and other controls. For second-lien misreporting, loan originator fixed effects explain a larger proportion of the second-lien misreporting variation than do underwriter fixed effects. The regression that includes all controls with CBSA-quarter fixed effects (but neither originator nor underwriter fixed effects) yields an of 0.10. Adding originator, but not underwriter fixed effects, yields an of 0.152, compared to 0.129 when adding only underwriter fixed effects. This suggests that second-lien misreporting seems to be more aligned with originator practices than with underwriter practices. Nevertheless, since underwriter fixed effects explain additional variation beyond originator fixed effects ( of 0.168), second-lien reporting may also be influenced by the underwriter. For appraisal overstatement and owner occupancy misreporting, Table 5 shows that the originator and underwriter fixed effects do not explain much of the misreporting. These types of misreporting did not vary widely across originators and underwriters.

Determinants of misreporting

| Unreported second | Occupancy misreporting | Appraisal overstatement | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Adj. | Relative increase (%) | Adj. | Relative increase (%) | Adj. | Relative increase (%) | ||||||

| Baseline | 0.100 | - | 0.087 | - | 0.085 | - | |||||

| w/Originator FE | 0.152 | 52.2 | 0.089 | 1.4 | 0.086 | 1.7 | |||||

| w/Underwriter FE | 0.129 | 29.1 | 0.087 | 0.1 | 0.085 | 0.4 | |||||

| w/Originator and | 0.168 | 68.2 | 0.089 | 1.5 | 0.086 | 1.8 | |||||

| Underwriter FE | Sample size | 1,726,075 | |||||||||

| Unreported second | Occupancy misreporting | Appraisal overstatement | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Adj. | Relative increase (%) | Adj. | Relative increase (%) | Adj. | Relative increase (%) | ||||||

| Baseline | 0.100 | - | 0.087 | - | 0.085 | - | |||||

| w/Originator FE | 0.152 | 52.2 | 0.089 | 1.4 | 0.086 | 1.7 | |||||

| w/Underwriter FE | 0.129 | 29.1 | 0.087 | 0.1 | 0.085 | 0.4 | |||||

| w/Originator and | 0.168 | 68.2 | 0.089 | 1.5 | 0.086 | 1.8 | |||||

| Underwriter FE | Sample size | 1,726,075 | |||||||||

This table compares the adjusted s obtained from OLS regressions of the misreporting indicators on loan-level controls and different combinations of originator and underwriter fixed effects. Underwriter information comes from Bloomberg. Only loans belonging to MBS deals in which one main underwriter is listed are considered. The variables Unreported second, Occupancy misreporting, and Appraisal overstatement are defined in Table 2. The complete regressions are shown in the Internet Appendix.

Determinants of misreporting

| Unreported second | Occupancy misreporting | Appraisal overstatement | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Adj. | Relative increase (%) | Adj. | Relative increase (%) | Adj. | Relative increase (%) | ||||||

| Baseline | 0.100 | - | 0.087 | - | 0.085 | - | |||||

| w/Originator FE | 0.152 | 52.2 | 0.089 | 1.4 | 0.086 | 1.7 | |||||

| w/Underwriter FE | 0.129 | 29.1 | 0.087 | 0.1 | 0.085 | 0.4 | |||||

| w/Originator and | 0.168 | 68.2 | 0.089 | 1.5 | 0.086 | 1.8 | |||||

| Underwriter FE | Sample size | 1,726,075 | |||||||||

| Unreported second | Occupancy misreporting | Appraisal overstatement | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Adj. | Relative increase (%) | Adj. | Relative increase (%) | Adj. | Relative increase (%) | ||||||

| Baseline | 0.100 | - | 0.087 | - | 0.085 | - | |||||

| w/Originator FE | 0.152 | 52.2 | 0.089 | 1.4 | 0.086 | 1.7 | |||||

| w/Underwriter FE | 0.129 | 29.1 | 0.087 | 0.1 | 0.085 | 0.4 | |||||

| w/Originator and | 0.168 | 68.2 | 0.089 | 1.5 | 0.086 | 1.8 | |||||

| Underwriter FE | Sample size | 1,726,075 | |||||||||

This table compares the adjusted s obtained from OLS regressions of the misreporting indicators on loan-level controls and different combinations of originator and underwriter fixed effects. Underwriter information comes from Bloomberg. Only loans belonging to MBS deals in which one main underwriter is listed are considered. The variables Unreported second, Occupancy misreporting, and Appraisal overstatement are defined in Table 2. The complete regressions are shown in the Internet Appendix.

4.4 Why are appraisals overstated?

Our analysis above shows that it is much more common for appraisals to be substantially above AVM model values than the opposite, and that these appraisal overstatements are strongly related to future loan performance. This pattern could be due to: (1) appraisers doing their best but making random mistakes in their appraisals, or (2) appraisers targeting the expectations of loan officers and thus biasing their appraisals upward. To examine which of these explanations is more prevalent, we examine refinances. With purchases, which are at arm's length, the buyer has an incentive to purchase at a low price. With refinances, in contrast, the price of the house depends solely on the appraisal. If appraisers are generally trying to please loan officers, then we should see more inflated appraisals for refinances. Among refinances, appraisal inflation might be largest among cash-out refinances, where the buyer's goal is to not only repay the previous debts on the property but also maximize the loan value taken. The loan officer may also have an incentive to maximize the loan size, as his or her commission is a function of the dollar value of the loan.

As shown in Table 2, appraisal overstatements are significantly more common in refinances. In panel A of Table 6, we estimate logit regressions for the frequency of appraisal overstatement (using the 20% threshold) and confirm that the higher levels of overstatements for refinances are not driven by loan characteristics. Appraisals in refinances are 74% more likely to be overstated than purchases. Additionally, we find that cash-out loan appraisals are more likely to be overstated than term refinance loan appraisals (odds ratio of 1.81 compared to 1.57, different at the 1% level).

Appraisal overstatements in refinances

| Panel A: Appraisal overstatement and refinances | ||

|---|---|---|

| Appraisal Overstatement | ||

| Refinance | 1.74*** | |

| (39.56) | ||

| Cashout refinance | 1.81*** | |

| (42.09) | ||

| Term/rate refinance | 1.57*** | |

| (28.80) | ||

| Controls | yes | yes |

| CBSA × Quarter FE | yes | yes |

| Observations | 2,575,484 | 2,560,060 |

| Pseudo | 0.09 | 0.09 |

| Panel A: Appraisal overstatement and refinances | ||

|---|---|---|

| Appraisal Overstatement | ||

| Refinance | 1.74*** | |

| (39.56) | ||

| Cashout refinance | 1.81*** | |

| (42.09) | ||

| Term/rate refinance | 1.57*** | |

| (28.80) | ||

| Controls | yes | yes |

| CBSA × Quarter FE | yes | yes |

| Observations | 2,575,484 | 2,560,060 |

| Pseudo | 0.09 | 0.09 |

| Panel B: Delinquencies and appraisal overstatements | ||

|---|---|---|

| Delinquent | ||

| Appraisal overstatement × LTV5 | 1.25*** | |

| (22.85) | ||

| Appraisal overstatement | 1.34*** | 1.16*** |

| (46.57) | (15.68) | |

| Controls | yes | yes |

| CBSA × Quarter FE | yes | yes |

| Observations | 2,576,423 | 2,576,423 |

| Pseudo | 0.25 | 0.25 |

| Panel B: Delinquencies and appraisal overstatements | ||

|---|---|---|

| Delinquent | ||

| Appraisal overstatement × LTV5 | 1.25*** | |

| (22.85) | ||

| Appraisal overstatement | 1.34*** | 1.16*** |

| (46.57) | (15.68) | |

| Controls | yes | yes |

| CBSA × Quarter FE | yes | yes |

| Observations | 2,576,423 | 2,576,423 |

| Pseudo | 0.25 | 0.25 |

This table shows the odds ratios of logit regressions in which the dependent variable is Appraisal overstatement or Delinquent. Refinances are split into cash-out refinances and term refinances. Appraisal overstatement × LTV5 captures appraisal overstatements for loans that have five-unit LTVs. The regression controls for reported second liens, reported nonowner occupied, low/no doc loans, loans used for refinancing, the borrower's credit score, loan amount, LTV, interest rate at origination, presence of a prepayment penalty, adjustable-rate loans, and complex loans. All regressions include core-based statistical area (CBSA) times quarter of origination fixed effects (CBSA × Quarter FE). Standard errors are clustered by CBSA × quarter of origination. The complete regressions are reported in the Internet Appendix. z-statistics are presented in parentheses. , , .